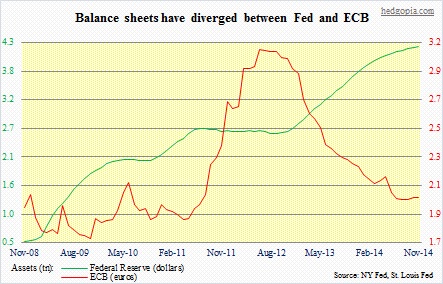

- Balance sheets have diverged between Fed and ECB

- As eurozone economy/inflation fall short, ECB under pressure to do QE

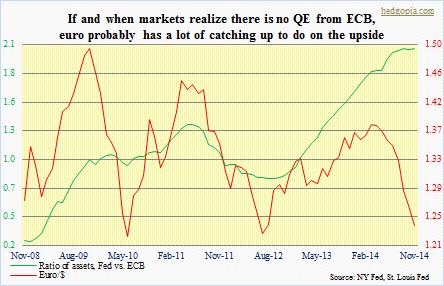

- If there is no QE from ECB, euro probably has a lot of catching up to do on the upside

There are several factors driving currency values – ranging from the amount of sovereign debt to inflation to interest rates to the current account. Add central-bank activity to the list. Post-financial crisis, central banks have stayed extra accommodative. In jurisdictions such as the eurozone, the U.K., Japan and of course the U.S., short rates are already so low there is effectively not much room to go any lower. Hence the unconventional methods such as quantitative easing. So where a nation is in its QE life can impact its currency.

Back in 1Q14, real GDP rather unexpectedly shrank in the U.S., followed by a quick snapback. Late last year, the Fed began to taper its monthly $85bn purchases of treasuries and mortgage-backed securities (QE3 is now done). As the economy was holding up just fine, markets began to price in a Fed interest-rate hike next year. The dollar bottomed in May this year. Across the Atlantic, it was a different story. The eurozone economy was – and is – still tentative. Inflation continues to drop.

One crucial difference between the two central banks was that ECB assets peaked at €3.1tn in June 2012 even as the Fed was getting ready for QE3. As a result, the ratio between the two took off – from lower left to upper right. The euro followed the ratio until the former peaked in March this year. Growth really has not picked up in the eurozone. And long rates have just collapsed. Mario Draghi, ECB president, drops a hint here and there that more stimulus is in the making – the press conference yesterday morning being one example. So markets are ready – for QE, that is. That is the reason why the two lines (in the chart above) have diverged. Expectations of a low – or lower – euro are written all over that divergence.

Here is the thing. As was discussed yesterday, if ever markets (1) lose patience with Draghi, (2) realize that there is not going to be QE, or (3) buy the QE rumor, and sell the news, the red line in the chart above has a lot of catching up to do.