The earnings season is upon us. The bar is low. With the S&P 500 sideways in recent weeks after a massive rally since last October, better results can help the index push through short-term resistance, but building on the gains will be tough, as bearish sentiment has collapsed.

The March-quarter earnings season begins in earnest later this morning. Customarily, financials will get the ball rolling, with results from JP Morgan (JPM), Citigroup (C) and Wells Fargo (WFC) in the dock. Leading into this, the revision trend is decidedly down. Estimates for all these three are lower from even a week ago.

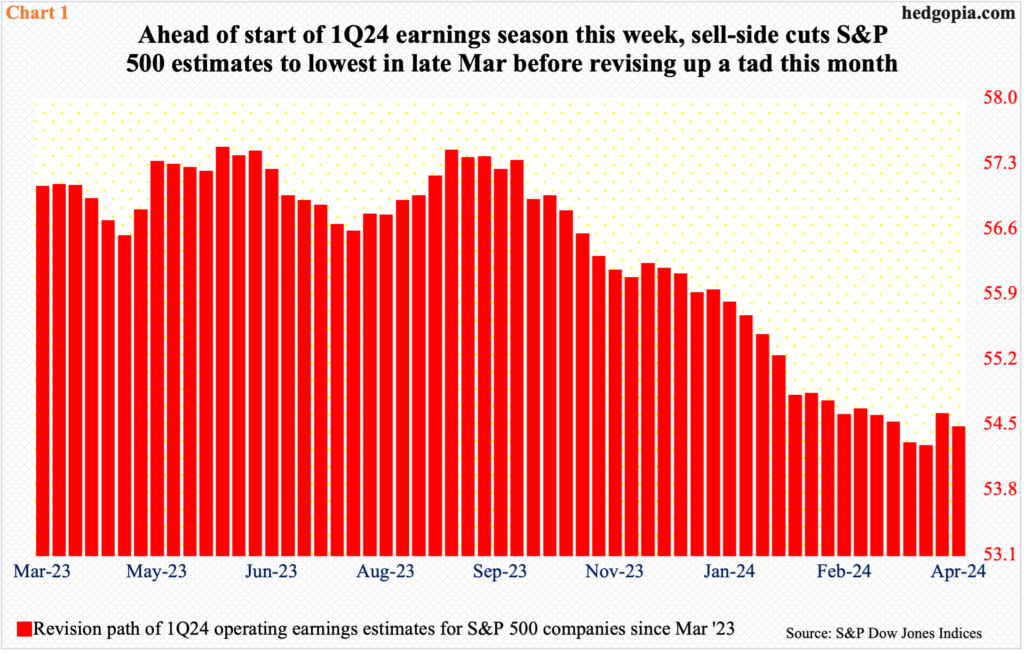

This is also true for the entire S&P 500. As of Tuesday, operating earnings estimates for these companies stood at $54.45 – up slightly from $54.25 as of March 27th but down from a high of $57.45 as of May 30th last year (Chart 1).

Once again, the sell-side habitually has lowered the bar ahead of the season.

Stocks act as if they are low enough the companies in the aggregate will be able to meet/beat.

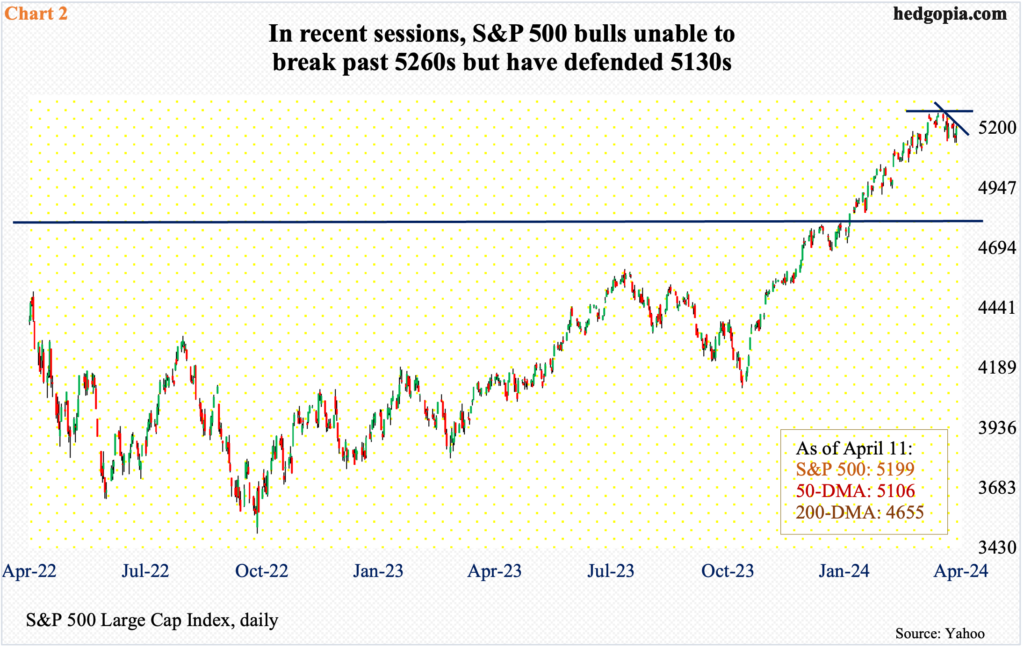

The S&P 500 peaked on March 28th at 5265. In three sessions between March 21st and April 1st, the large cap index touched 5260s but only to then retreat. Equity bears, however, have not been able to make much of the subsequent drop.

On both Wednesday and Thursday this week, bids showed up at 5139, with the latter session ending up 0.7 percent to 5199. Bulls stepped up to the plate just above the 50-day; the last time the index closed below the average was early November last year, with an important bottom having been reached only a few sessions ago in October.

As things stand, unless earnings disappoint big time, bulls should fight tooth and nail to save the average. In fact, the S&P 500 has trended lower along a line month-to-date, with Thursday closing right on/underneath it (Chart 2). Concurrently, shorter-term averages (10, 20) are on the verge of a cross-down, which, should one unfold, will embolden the bears.

Hence the importance of this morning’s results from the banks. A trendline breakout will mean the bulls will get another shot at 5260s. And this would have come at a time when there are fewer and fewer bears around.

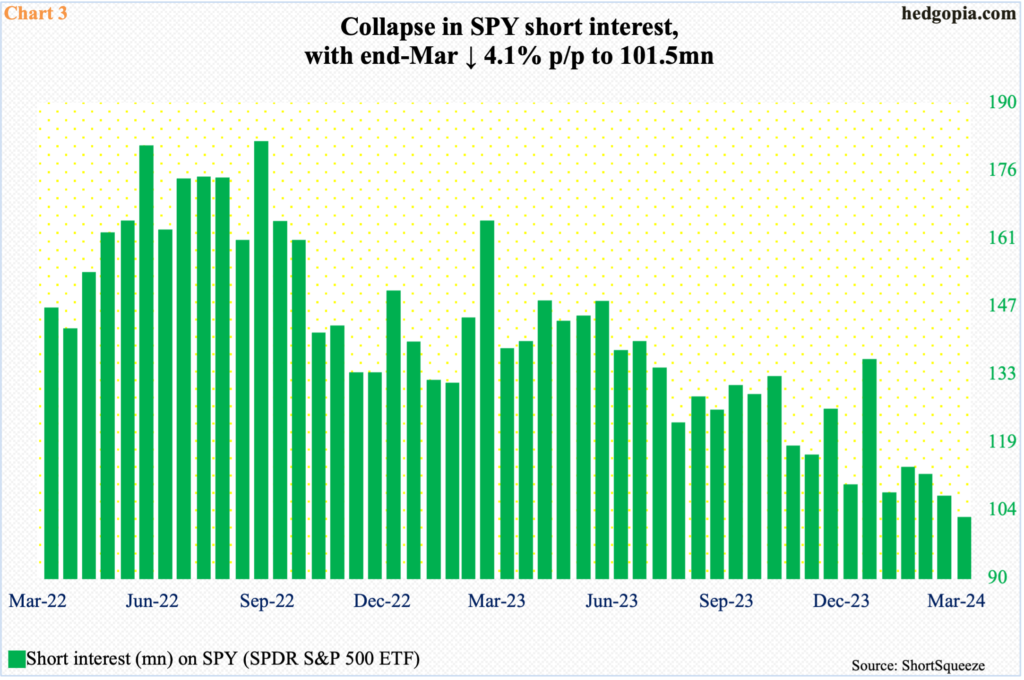

At the end of March, short interest on SPY (SPDR S&P 500 ETF) was only 101.5 million (Chart 3). This is nothing but an absolute collapse in bearish sentiment. At the middle of September 2022, short interest was 180.5 million – shortly before the S&P 500 reached a major bottom in October. This has been quite a squeeze since.

This also means that the bulls will not be benefiting from a squeeze tailwind going forward; or, if they did, it will be increasingly trivial.

Thanks for reading!