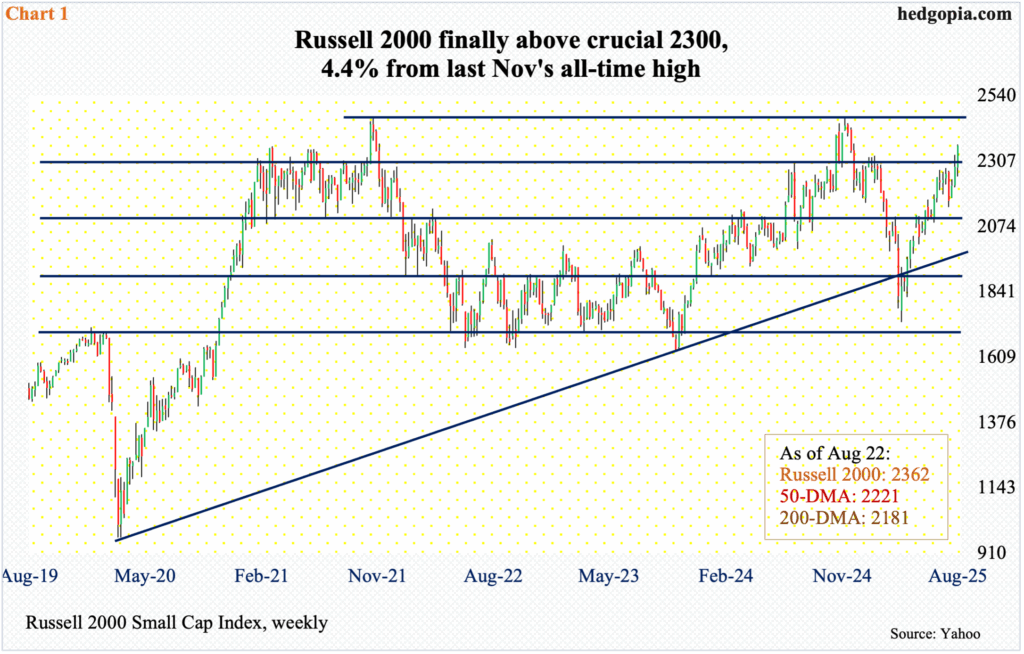

After multiple attempts, the Russell 2000 has finally pushed through 2300 – on rate-cut hopes. This sentiment is also evident in the recent rise in small-business optimism, although it is not yet translated into increased job openings. Uncertainty remains – the biggest one being whether all this flows through to earnings which are expected to surge next year.

Small-cap bulls have finally achieved a close above 2300 on the Russell 2000. This level has attracted both bulls and bears going back to February 2021, and since July last year most recently.

Last week, the index rose 3.3 percent to 2362. Seven sessions ago, it had a similar breakout, but it turned out to be false. Last week’s looks like it may have staying power – for now. The small cap index needs to rally another 4.4 percent before it reaches last November’s intraday high of 2466, which narrowly edged past the prior high of 2459 from November 2021 (Chart 1).

There are a couple of things to consider. One, the Russell 2000 remains overbought – on the weekly in particular, as it bottomed at 1733 in April. Two, if it manages to rally toward its highs, failure risks are high, as last week’s rally was predicated on hopes of persistently lower interest rates.

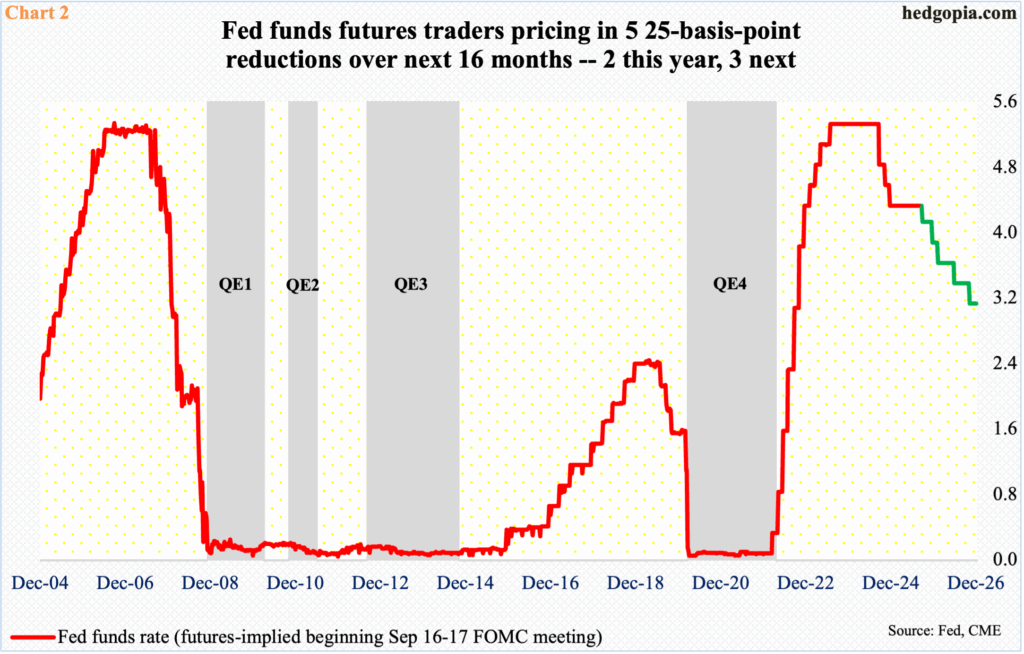

Federal Reserve Chairman Jerome Powell dropped strong hints at Jackson Hole last Friday that a rate cut may be warranted. The FOMC (Federal Open Market Committee) next meets on September 16-17. This will be the first cut since last December; back then, the fed funds rate was lowered by 100 basis points over three meetings, beginning with a 50 in September, to a range of 425 basis points to 450 basis points.

In the futures market, traders are currently betting with 87 percent probabilities that a 25-basis-point easing is locked in for next month, followed by another in December, then three more next year. Altogether, they are pricing in cuts equaling 125 basis points in the next 16 months (Chart 2).

The central bank operates with a dual mandate – maximum employment and price stability. July’s rather meager jobs report, coupled with sharp downward revisions for May and June, gives the FOMC plenty of room to begin to cut. But the other side of the coin is not fully cooperating. Inflation – both CPI (consumer price index) and PCE (personal consumption expenditures) – have been trending higher the last four to five months and are around three percent. The Fed has a stated goal of two percent. Plus, producer prices have also been firming up of late. The uncertainty emanating out of tariffs continues to bug both consumers and businesses.

With this as a background, a 25-basis-point cut next month may not necessarily mark the start of a sustained easing cycle, which has often been the case in the past. Last Friday’s reaction by small-cap bulls rallying the Russell 2000 3.9 percent, however, seems to be readying for much lower rates, which would then help shift the economy into higher gear. Small-cap businesses by nature have a much higher exposure to the domestic economy than their large-caps cousins which are also exposed internationally.

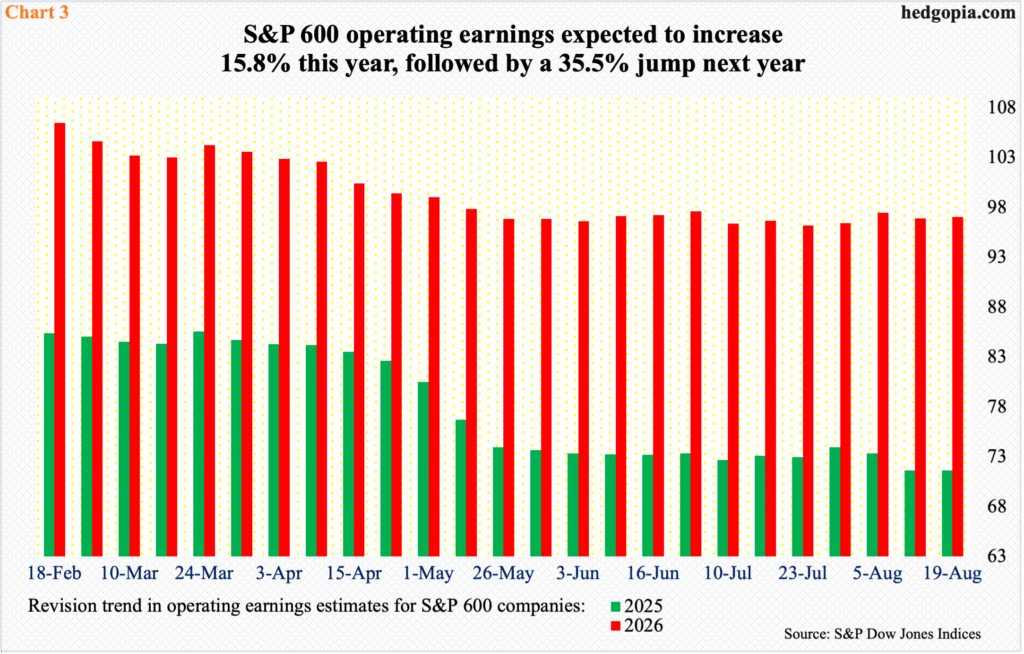

This scenario is also evident in how the sell-side expects operating earnings for S&P 600 companies to evolve next year. For 2025, as of last Tuesday, they were modeling in $71.66, which is substantially lower than the $102.88 expected as of May 2nd last year. However, next year’s estimates, although down from $106.48 expected as of February 18th, have gone sideways around $97 the past three months (Chart 3). If it comes to pass, next year’s earnings would have grown north of 35 percent, versus this year’s estimate of just under 16 percent. A lot of things must go right for small-cap companies to realize this optimism.

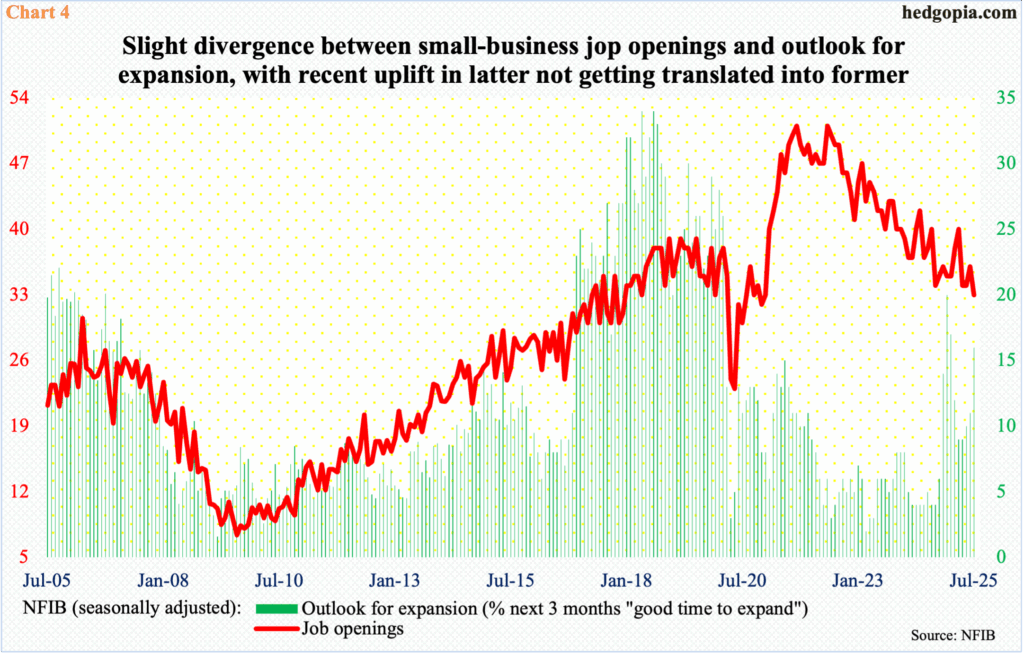

Speaking of optimism, small businesses are beginning to show some of it in recent months. The NFIB (National Federation of Independent Business) outlook for expansion sub-index jumped five points month-over-month in July to 16. This was a seven-month high, having dropped to nine in both March and April (Chart 4).

This is well and good, but this optimism is not getting translated into actual job openings, which in July declined three points m/m to 33, which was the lowest reading since December 2020.

Last week’s reaction by the bulls is an indication that the risk is worth taking at this point.

With five sessions to go this month, the Russell 2000 is up 6.8 percent. After April’s bottom, it would have now rallied for four months in a row. And this is coming with full support from leverage.

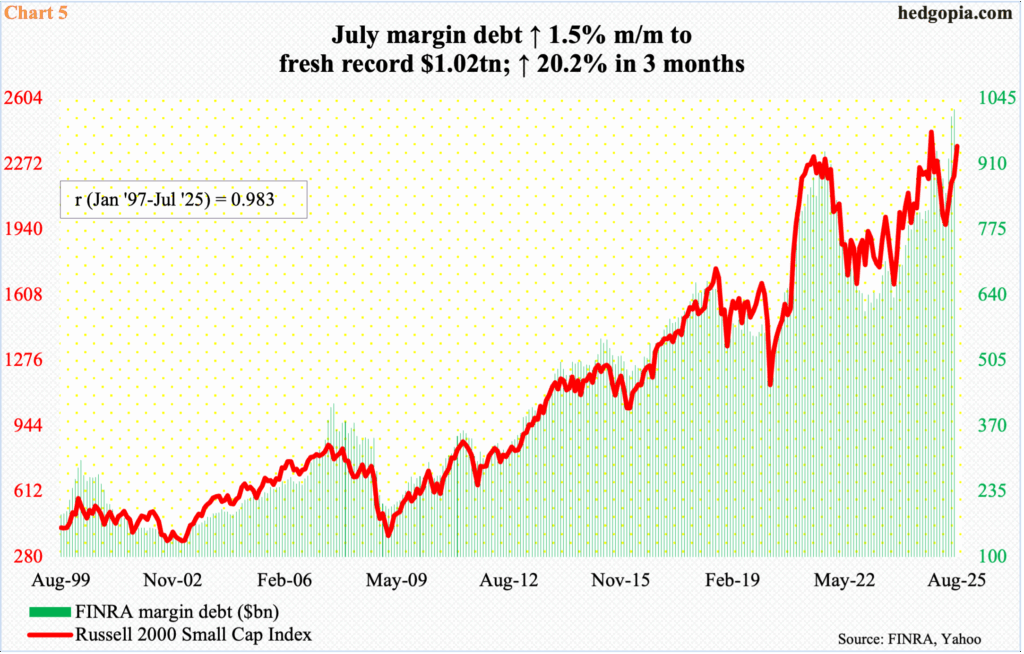

In April, FINRA margin debt hit a six-month low of $850.6 billion, before rising the next three months, reaching a fresh high of $1.02 trillion in July. This reflects the prevailing sentiment of risk-on. Small-caps historically are the same away. The Russell 2000 and margin debt do have a coefficient correlation of 0.98 going back to January 1997 (Chart 5). If this relationship holds, margin debt must have grown by a decent chunk this month.

This should also give the bulls hope that last November’s high is within striking distance. Even if that were to be the case, ultimately, they would need the FOMC’s help in sustaining those gains. Last week’s 2300 breakout is a step in the right direction technically, but that needs to be followed by good news fundamentally. And this is where things are a little uncertain currently.

Thanks for reading!