Following futures positions of non-commercials are as of June 24, 2025.

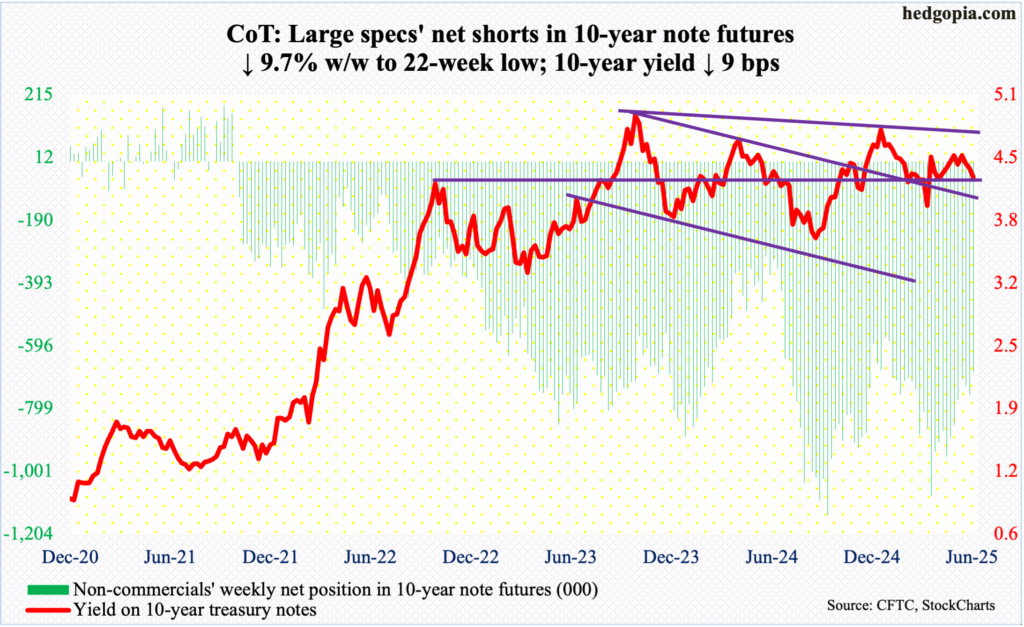

10-year note: Currently net short 680.1k, down 72.8k.

Futures traders boosted rate-cut expectations this year to three this week – one each in September, October and December. For a while, they had been stuck at two 25-basis-point reductions. In last week’s meeting, the fed funds rate was left steady at a range of 425 basis points to 450 basis points.

Traders’ increased optimism probably had less to do with economic data and more with rumors that President Donald Trump could soon name a replacement for Jerome Powell, whose term as Federal Reserve chair expires next May (although his term as governor does not expire until 2028).

Trump has repeatedly called for lower rates, blaming Powell, who by the way was nominated by Trump himself eight years ago, for not doing so. Markets are betting that a so-called “shadow chair” could help influence interest rate policy.

The irony in all this is that the Federal Open Market Committee (FOMC) is made up of 12 members – seven governors, New York Fed president and four of the remaining 11 district banks, who serve one-year terms on a rotating basis. They all have a vote.

In this scenario, even if the upcoming nomination by Trump turns out to be a loyalist, it remains to be seen if the person continues to act that way in decision-making once inside the Eccles Building. Markets hope not.

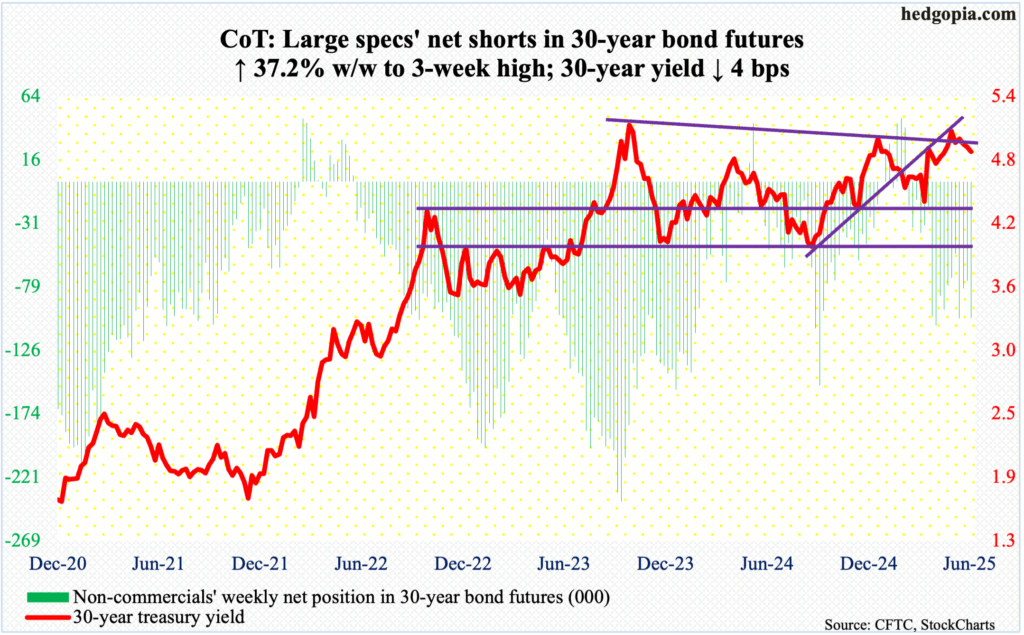

30-year bond: Currently net short 101.8k, up 27.6k.

Major US economic releases for next week are as follows. Markets are closed Friday for observance of Independence Day!

Job openings (JOLTs, May) and the ISM manufacturing index (June) are on tap for Tuesday.

Non-farm job openings in April increased 191,000 month-over-month to 7.4 million. Last November, openings were eight million and peaked at 12.1 million in March 2022.

In May, manufacturing activity edged down two-tenths of a percentage point m/m to 48.5 percent – a six-month low. The back-to-back expansionary readings of just north of 50 percent in January and February this year followed 26 consecutive months of contraction.

Thursday brings the employment report (June), durable goods orders (May, revised) and the ISM services index (June).

In the first five months this year, the economy created an average 124,000 non-farm jobs. Should this pace continue through the rest of the year, this would represent a weak performance versus the monthly average of 168,000 in 2024, 216,000 in 2023 and 380,000 in 2022.

Orders for non-defense capital goods ex-aircraft – proxy for business capex plans – firmed up 1.7 percent m/m to a seasonally adjusted annual rate of $76 billion. This was the highest since December 2022, with the series having peaked at $78.1 billion in August that year.

Non-manufacturing activity declined 1.7 percentage points m/m in May to 49.9 percent, which was the first sub-50 reading in 11 months.

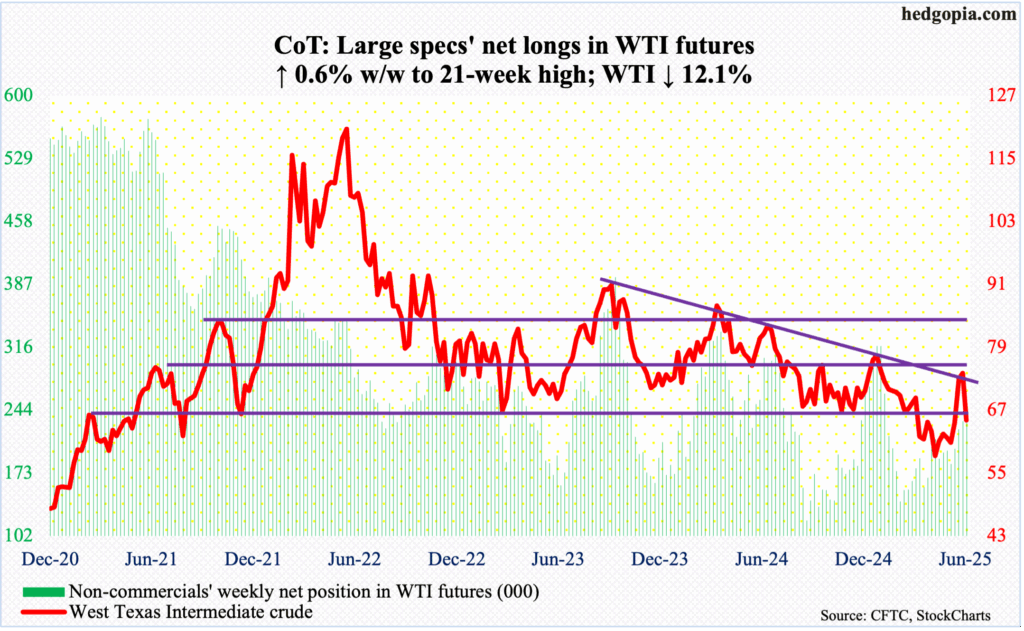

WTI crude oil: Currently net long 233.4k, up 1.4k.

West Texas Intermediate crude reversed hard this week, down 12.1 percent to $65.07/barrel. At Monday’s intraday high of $78.40, it was on course for a fourth straight up week, but the session ended up reversing hard, closing at $68.51, right at the 200-day ($68.47). The average was breached in the very next session, closing the week between the 200- and 50-day ($63.62).

This was a nasty reversal and came right on trendline resistance from September 2023 when the crude peaked at $92.48. There is horizontal support at $65-$66, which is now vulnerable. In all probability, money that bet on closure of/disturbance at the Strait of Hormuz either left this week or are left with holding the bag.

In the right circumstances, oil bears are probably eyeing horizontal support at $55, which goes back a couple of decades. On 9 April, WTI, having peaked at $79.39 on 15 January, bottomed at $56.06, which could be in play in the weeks ahead.

In the meantime, US crude production in the week to June 20th increased 4,000 barrels per day week-over-week to 13.435 million b/d; output has come under slight pressure since registering a record 13.631 mb/d in the week to December 6th last year. Crude imports increased as well, up 440,000 b/d to 5.9 mb/d. Stocks of crude, gasoline, and distillates went the other way, respectively down 5.8 million barrels, 2.1 million barrels and 4.1 million barrels to 415.1 million barrels, 227.9 million barrels and 105.3 million barrels. Refinery utilization rose 1.5 percentage points to 94.7 percent.

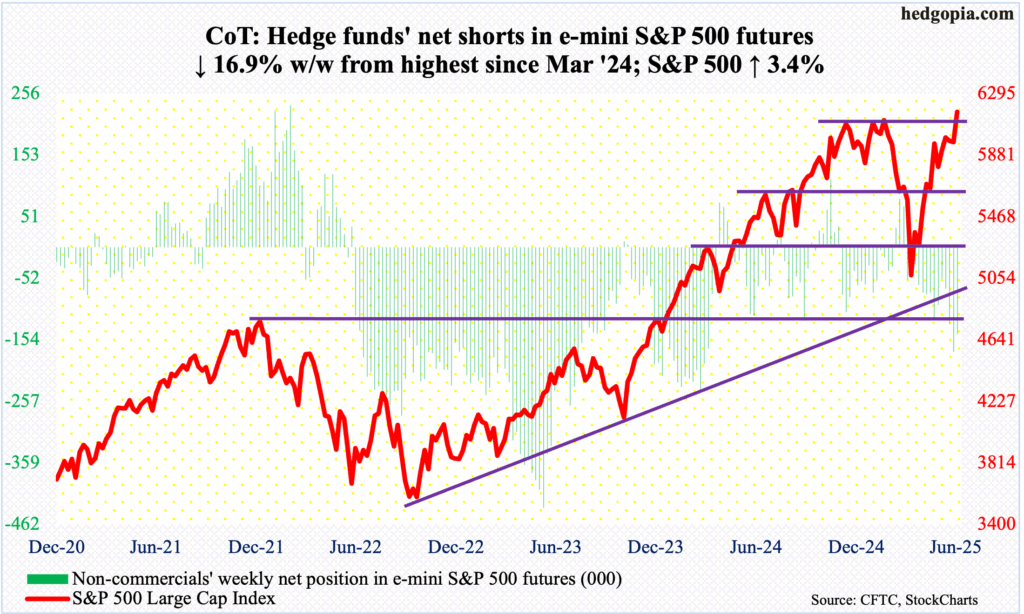

E-mini S&P 500: Currently net short 144.8k, down 29.4k.

Equity bulls deserve kudos for pulling this off. Between 19 February (6147) and 7 April (4835), the S&P 500 tumbled 21.3 percent. In the subsequent weeks, the large cap index has not only managed to erase those losses but also break out to a new high. This week, it rallied 3.4 percent to 6173, with a new intraday high of 6188.

With this, for the first time since last July, the daily RSI (70.21) has crossed 70. This shows how strong the current momentum is, but this is also an area where the bulls can find it difficult to sustain positive momentum. In fact, they should consider it healthy should the S&P 500 come under pressure but only to be met with buying interest at 6120s-6140s, or 6050s below that.

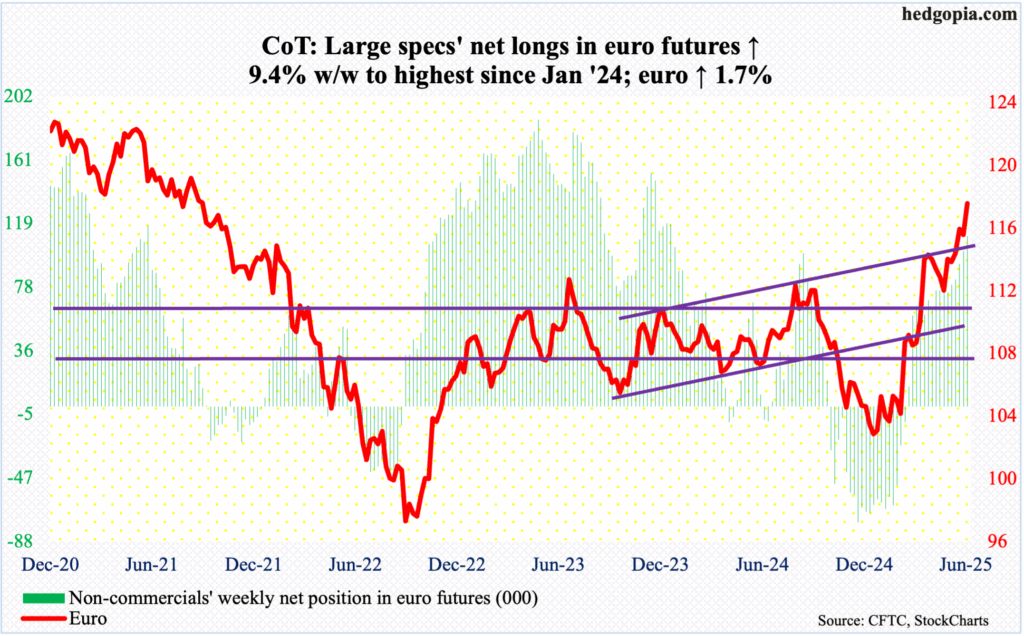

Euro: Currently net long 111.1k, up 9.6k.

There is no stopping the euro, fully cashing in on the greenback’s woes. This week, the euro shot up 1.7 percent to $1.1719, which is the highest intraday print since September 2021. Horizontal resistance at $1.16 goes back a couple of decades, and it finally gave way after a few tries, having rallied past the level intraday in the prior two weeks.

The euro not surprisingly remains extended. It has come a long way since early this year when it bottomed around $1.02s; earlier, the currency faced difficulty breaking through $1.12 last August and September, which it broke out of this April. The bulls now have another layer of support at $1.16, which should constitute an important breakout retest.

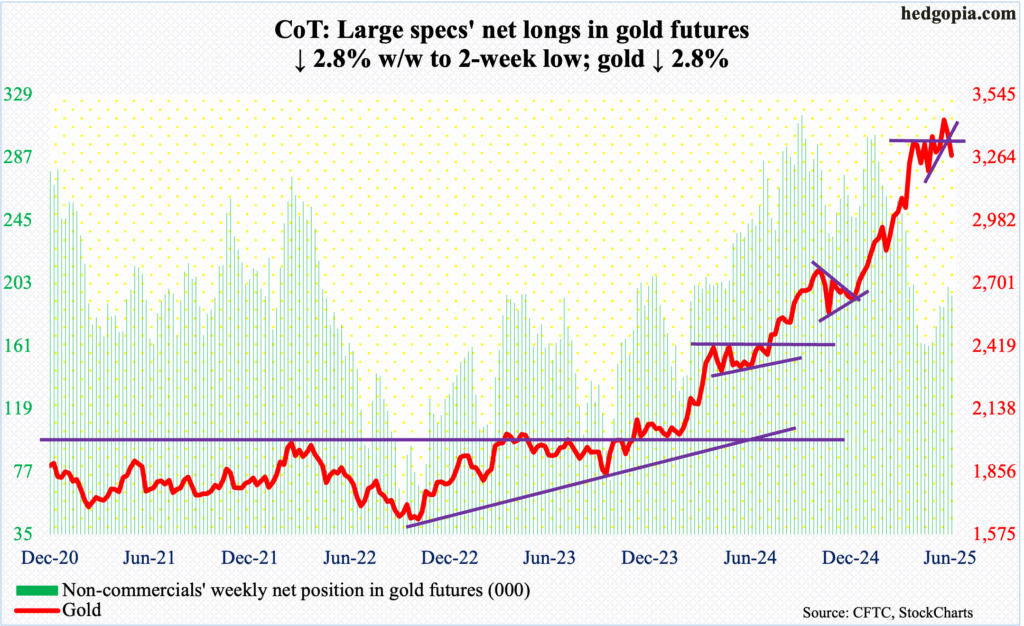

Gold: Currently net long 195k, down 5.6k.

The recent easing of tensions in the Middle East is taking the shine off gold, which lost 2.8 percent this week to $3,274/ounce. This was a second consecutive weekly loss for the metal.

Importantly, gold posted a fresh all-time high of $3,500 on 22 April, before going sideways. Throughout the 12-day war between Israel and Iran, the yellow metal was unable to surpass that high. This Friday, it lost the 50-day ($3,323).

Nearest support lies at $3,200.

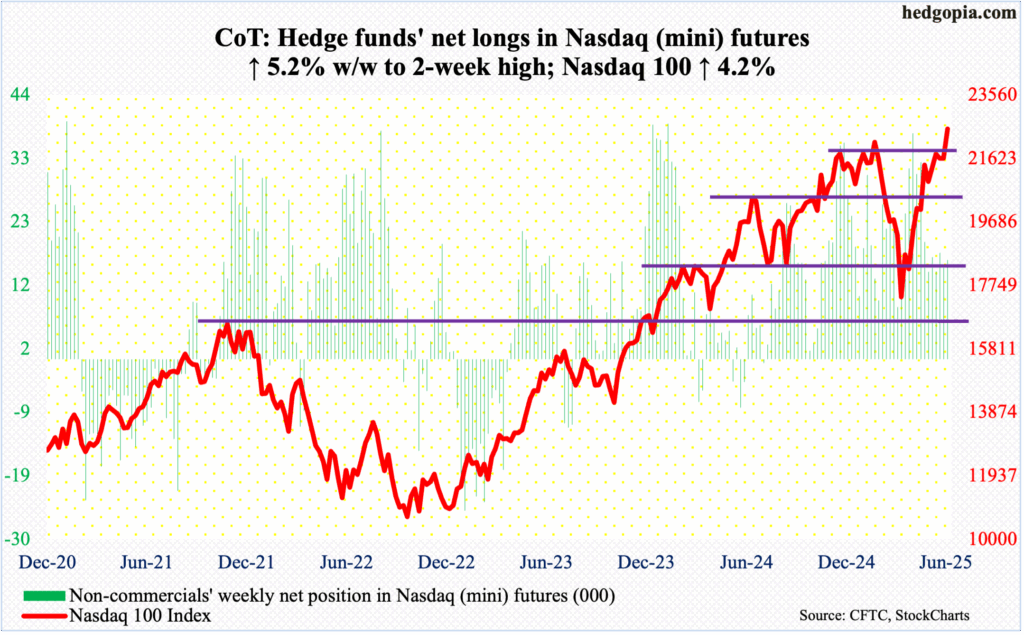

Nasdaq (mini): Currently net long 16.5k, up 815.

After two – even three – weeks of failure at 22100s, the Nasdaq 100 finally broke past the resistance this week to a fresh intraday high of 22603, closing the week up 4.2 percent to 22534.

Back on 19 February, the tech-heavy index hit 22223 and came under pressure, before dropping all the way to 16542 by 7 April. The recovery since that bottom has been very impressive, having come at a time of elevated trade and geopolitical tensions.

That said, participation could be better. In four successive trading sessions between the 6th and 11th this month, 86-87 percent of Nasdaq 100 stocks were above their 50-day. Friday, in a session the index posted a new high, only 75 percent were and were down two percentage points from Thursday’s.

The June-quarter earnings reporting season begins in a couple of weeks. Before that happens, odds favor a breakout retest at 22100s, which is a must-hold as far as the bulls are concerned.

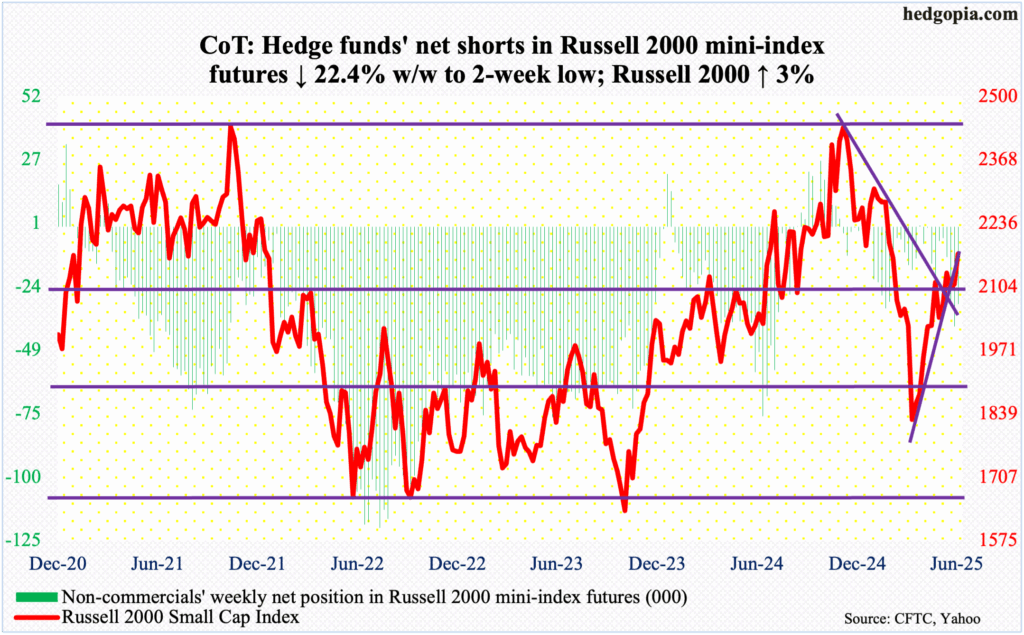

Russell 2000 mini-index: Currently net short 30.8k, down 8.9k.

The Russell 2000 is back at testing its 200-day (2174). On Friday, in fact, if the session high of 2189 held, the small cap index would have reclaimed the average, but it instead closed at 2173, up three percent for the week.

Unlike large-cap indices such as the S&P 500 and Nasdaq 100, which have now rallied to fresh highs, the Russell 2000 is nowhere near its. Last November’s new all-time high of 2466 just edged past the prior high of 2459 from November 2021. It then bottomed at 1733 on 9 April. The subsequent recovery stalled at 2100 for a few weeks before breaking out early this month. This was followed by increased buying interest at that level. This is positive. If small-cap bulls can keep this up, they will have a shot at 2300 in due course.

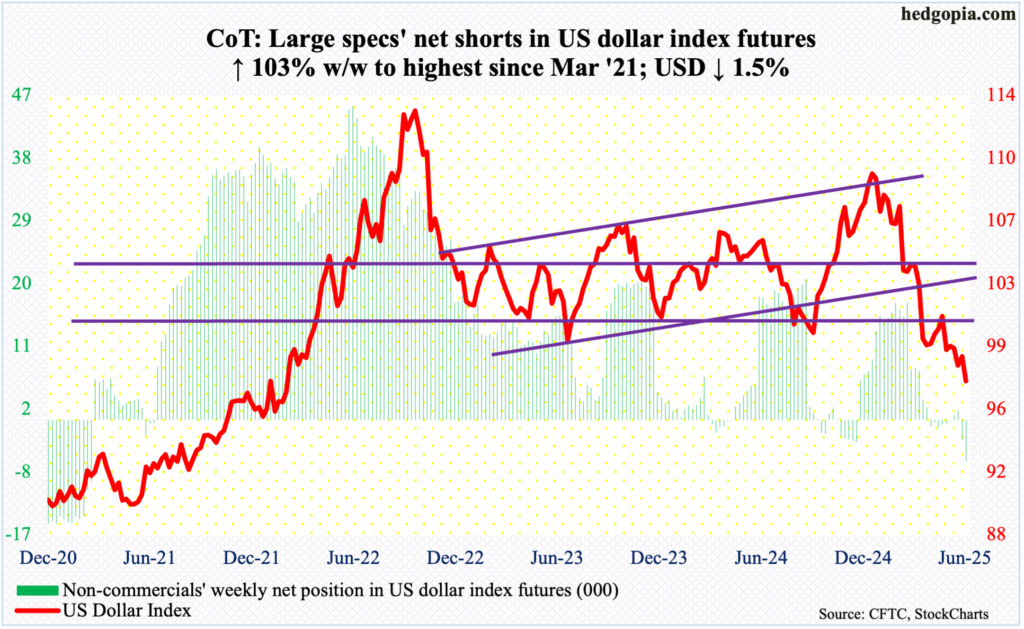

US Dollar Index: Currently net short 6k, up 3.1k.

The US dollar index cannot catch a break. With one session of trading left, it is down 2.1 percent in June. If this holds, this will represent a sixth down month in a row. On 12 January, the index tagged 110.18 and headed lower. This week, it gave back 1.5 percent to 97.27, breaching the low of 97.60s printed in three consecutive sessions between the 12th and 16th this month.

As awful as the decline has been this year, there is major support at 97 – or just underneath – which amounts to a rising trendline from the lows of April and May 2011.

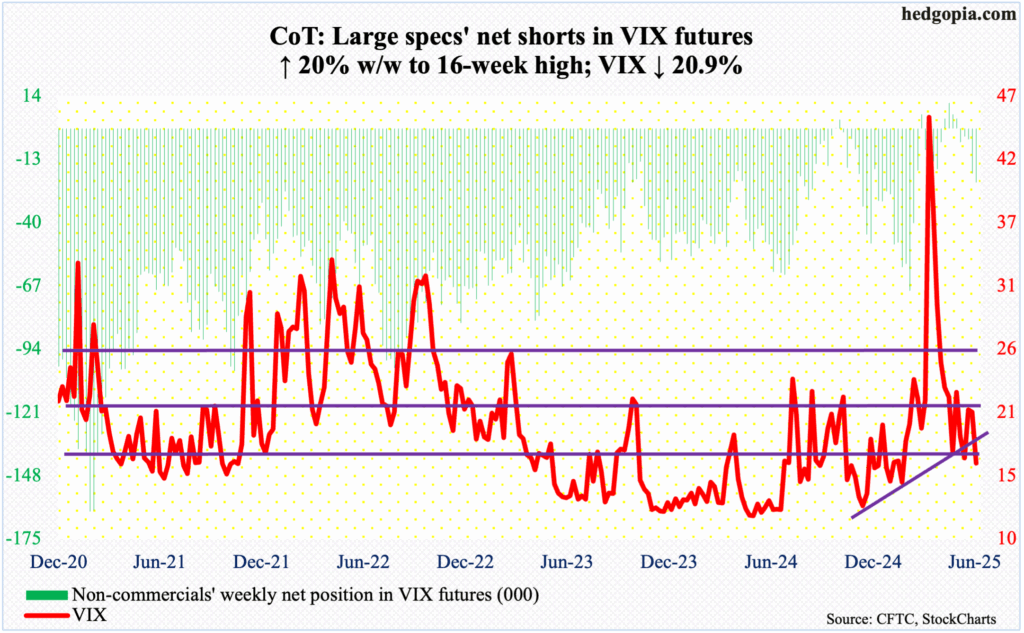

VIX: Currently net short 23k, up 3.8k.

VIX yielded 4.3 points this week to 16.32, essentially sitting on a rising trendline from last July on an intraday basis; on closing, however, the support has been breached. Non-commercials, in the meantime, further added to their net shorts in VIX futures; last week, they aggressively added to their holdings, and it paid off big this week.

Near-term, a drop to the 15 handle looks increasingly likely, with a worse-case scenario of 14.50s.

Thanks for reading!