Following futures positions of non-commercials are as of May 19, 2026.

10-year note: Currently net short 848.1k, up 66.9k.

The fed funds rate currently stands at a target of 350 basis points to 375 basis points. The benchmark rates have been left unchanged since last December when they were reduced by 25 basis points; this preceded a cut of similar magnitude in September and October. Earlier, the 10-year reached a cycle high 525 basis points to 550 basis points in July 2023, followed by cumulative cuts of 100 basis points over three meetings in 2024.

Even though the short rates have remained anchored just under four percent, the 10-year treasury yield has refused to go along, as it has rallied 40 basis points this year to 4.56 percent; in fact, these notes were yielding 4.69 percent intraday Tuesday before coming under pressure.

It is now increasingly getting clearer that the Federal Reserve will have to play a catch-up to the bond market. Until the start of the Iran war in late February, per CME FedWatch, traders were betting on a couple of quarter-point cuts this year. This has now vanished. Rather, traders are pricing in a well over 50 percent chance of a hike by December.

This week, the April 28-29 FOMC minutes showed that most officials indicated that “some policy firming” may be appropriate should disinflation stall. About that, on a headline and core basis, the CPI (consumer price index) rose 3.8 percent and 2.8 percent in the 12 months to April, with the former at a 35-month high and the latter the highest since last September. April’s PCE (personal consumption expenditures) inflation is due out Friday; in the 12 months to March, headline and core PCE jumped 3.5 percent and 3.2 percent respectively, setting a 33- and 28-month high, in that order. Core CPI and PCE have been above the Fed’s targeted two percent since April and March of 2021 respectively. That is five years!

Kevin Warsh, who was sworn in as new Fed chair on Friday, will be tested early on how he handles the situation. President Donald Trump, who appointed him, makes no bones about wanting lower rates. If Warsh tries to indulge, then the probabilities are very high that the 10-year decidedly marches toward five percent, which was last hit in October 2023. The next FOMC meeting is scheduled for June 16-17.

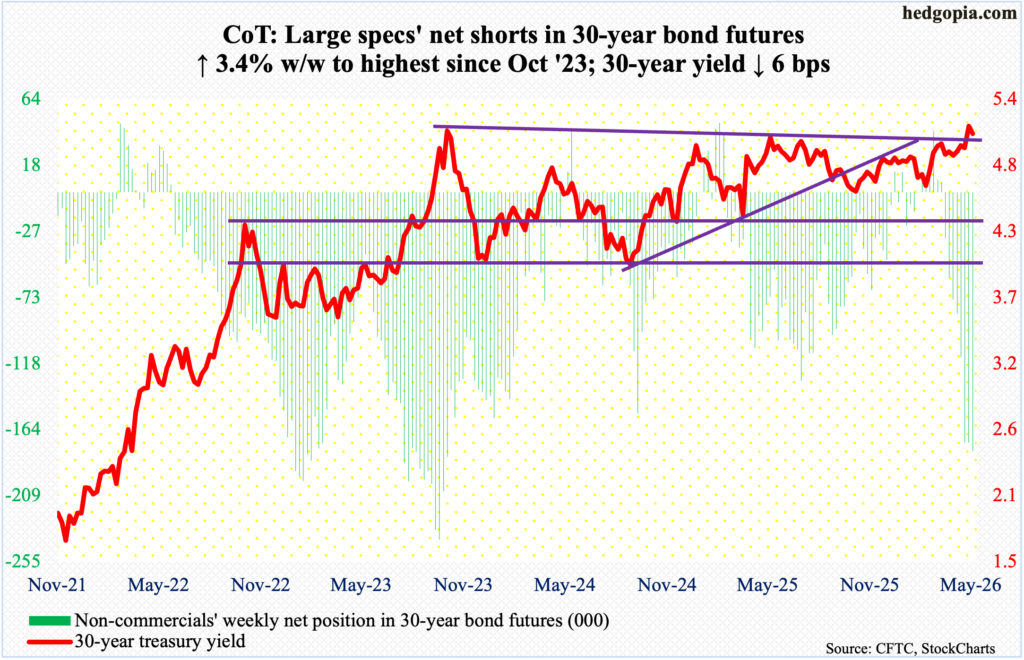

30-year bond: Currently net short 178.7k, up 5.8k.

Major US economic releases for next week are as follows. Markets are closed Monday for observance of Memorial Day holiday.

The S&P Case-Shiller home price index (March) is due out Tuesday. Nationally in February, home prices edged up 0.7 percent from a year ago. This was the slowest pace of appreciation in 32 months.

Durable goods orders (April) and new home sales (April) are scheduled for Thursday.

Orders for non-defense capital goods ex-aircraft – proxy for business capex plans – increased 3.4 percent month over month in March to a seasonally adjusted annual rate of $83 billion, which set a fresh record. From a year ago, orders jumped 9.5 percent.

March sales of new homes rose 7.4 percent m/m to 682,000 units (SAAR) – a three-month high. Last November’s 748,000 units set a 45-month high.

Friday brings GDP (1Q26, 2nd estimate), corporate profits (1Q26) and personal income/spending (April).

The advance estimate showed that real GDP in the March quarter grew two percent (SAAR).

From a year ago, corporate profits adjusted for inventory valuation and capital consumption jumped 9.6 percent in the December quarter to $4.35 trillion (SAAR) – a record.

In April last year, headline and core PCE respectively bottomed at 2.3 percent and 2.6 percent before trending higher.

WTI crude oil: Currently net long 144.3k, up 15.9k.

Since March 2 when West Texas Intermediate crude gapped up in response to the February 28 US-Israeli attack on Iran, it has persistently made lower highs and higher lows.

On March 9, the crude tagged a four-year high $119.48 and proceeded to set a lower high $117.63 on April 7, $110.93 on the 30th and $106 on the 15th this month. Down below, the March 2 low of $69.20 was followed by higher lows of $80.56 on April 17, $88.66 on the 6th this month and $94.73 this Friday. Consequently, a two-and-a-half-month pennant has resulted. This week, the crude dropped 7.9 percent to $97.07/barrel, with Friday’s low kissing the pennant support.

If it is a bullish pennant pattern, then this support should hold. Else, WTI can gravitate toward the nearest horizontal support at $91-$92. On the weekly in particular, the crude has room to head lower to unwind the overbought condition it is in. On February 27, WTI tagged $64.85 intraday before exploding higher in the subsequent sessions.

In the meantime, as per the EIA, US crude production in the week to May 15 decreased 8,000 barrels per day week over week to 13.702 million b/d; output registered a record 13.862 mb/d in the week to November 7 last year. Crude imports rose 115,000 b/d to six mb/d. As did stocks of distillates, which grew 372,000 barrels to 102.9 million barrels. Crude and gasoline inventory went the other way – down 7.9 million barrels and 1.5 million barrels respectively to 445 million barrels and 214.2 million barrels. Refinery utilization edged lower one-tenth of a percentage point to 91.6 percent.

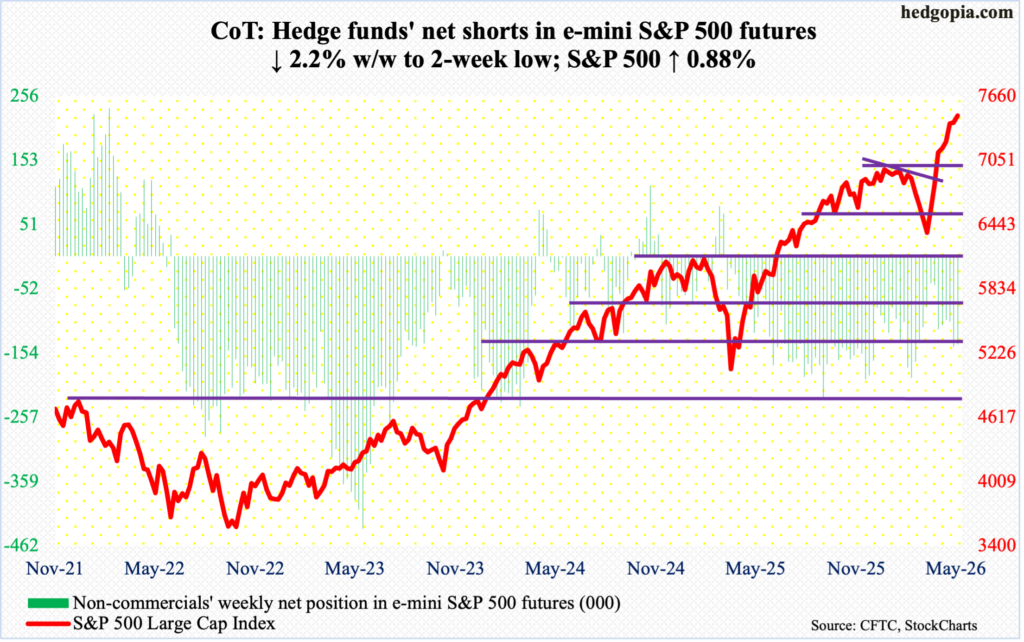

E-mini S&P 500: Currently net short 140.6k, down 3.2k.

Equity bears had an opportunity and did push the S&P 500 lower in the first two sessions, with the index down 2.4 percent from the all-time high of 7517 posted on the 14th through Tuesday’s session low of 7334. Bulls pounced on that low, managing to close the large cap index up 0.9 percent for the week to 7473. The only thing they are probably not happy about is how Friday evolved, as the session high 7506 was less than 11 points from the record registered six sessions before that, finishing with a daily shooting star.

On the weekly, however, it was an eighth consecutive up week. The S&P 500 earlier bottomed at 6317 on March 30, rallying 19 percent through the May 14 record. The index remains overbought but has been that way for a while now. So, the extended condition in and of itself is not a guarantee of an unwinding; that said, with each push higher, risks go up.

In the event of sustained downward pressure, 7270s is the first line of defense, followed by 7140s, and the all-important breakout retest just north of 7000.

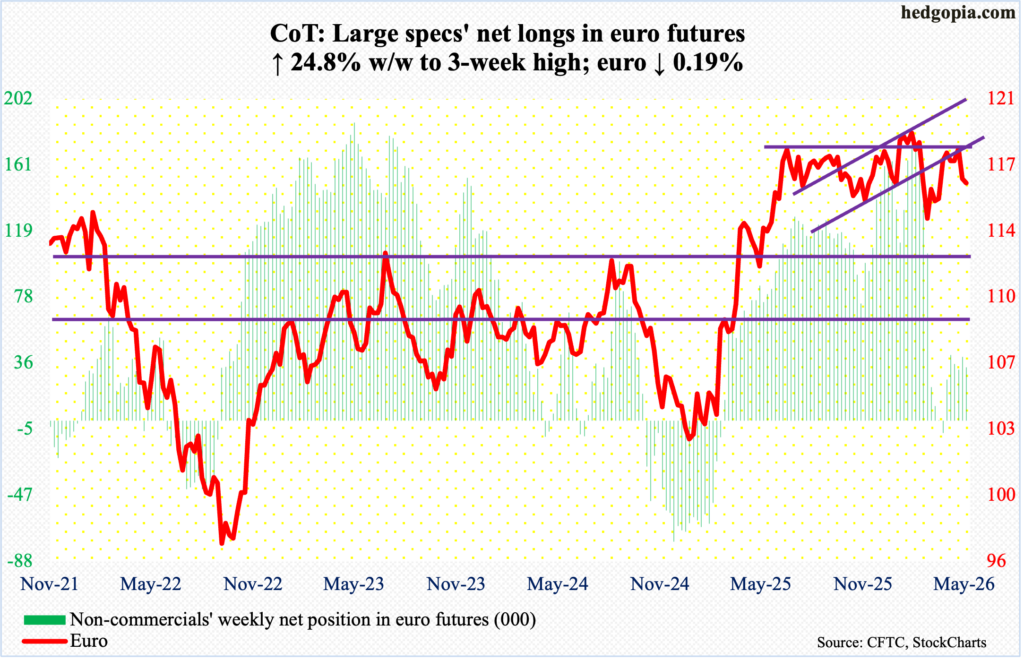

Euro: Currently net long 33.5k, down 6.7k.

Last Thursday and Friday, the euro sliced through the 200- and 50-day moving averages (respectively $1.168 and $1.166). This week, early attempts to reclaim the 50-day faced stiff opposition, as the currency ended down 0.2 percent for the week to $1.16.

Last week, after trying for five successive weeks to penetrate horizontal resistance at $1.18, bulls threw up their hands. For a year now, the euro has played ping pong between $1.14 and $1.18, with a four-and-a-half-year high $1.2083 posted on January 27. On March 13, it bottomed at $1.141.

The daily is beginning to get oversold, but $1.14 likely acts as a magnet in due course.

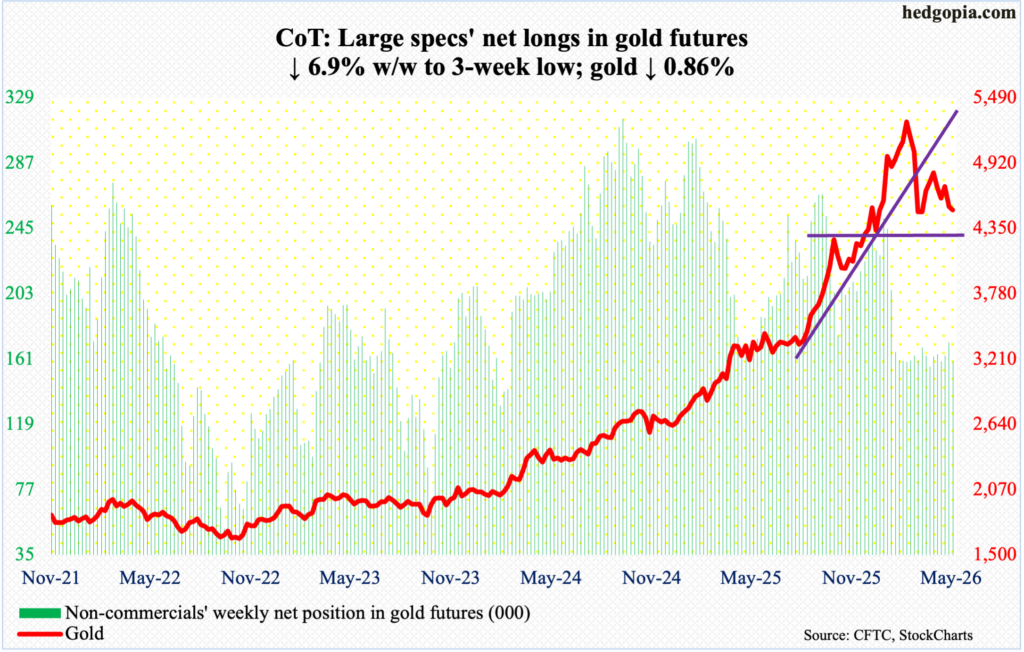

Gold: Currently net long 159.8k, down 11.8k.

The prospect of higher rates in the quarters ahead is beginning to sap bullish sentiment. This week, gold gave back 0.9 percent to $4,509/ounce. This was the fourth down week in five.

Earlier, gold’s all-time high was registered on January 29 at $5,608, before making lower highs, including $5,419 on March 2, $4,892 on April 17 and $4,774 on the 12th this month. Concurrently, the metal has remained sandwiched between the 50- and 200-day ($4,669 and $4,353 respectively), with the former falling and the latter rising.

As things stand, the 200-day is the path of least resistance, and this likely gets embraced by gold bugs. There is major support at $4,400, or just underneath.

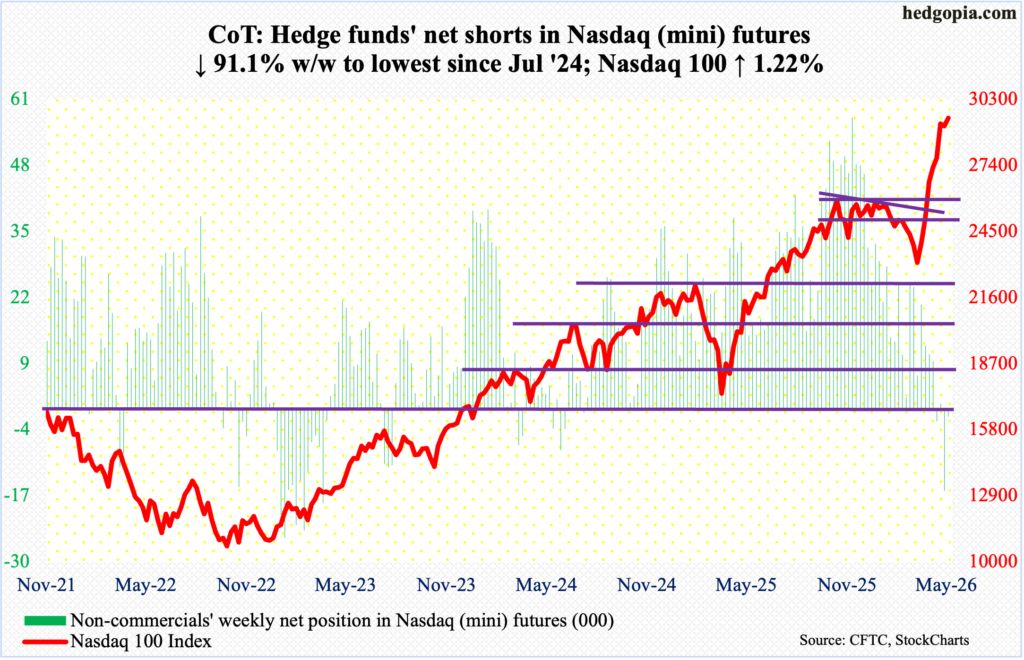

Nasdaq (mini): Currently net short 1.4k, down 14.6k.

Nvidia (NVDA) reported a beat-and-raise April quarter, and the stock failed to lift. It is a $5.2-trillion behemoth, already pricing in a lot of good news. Closing the week at $215.33, and an all-time high of $236.54 tagged on the 14th, there is major breakout retest at $211-$212. A breach will reverberate through all kinds of market-cap-weighted large-cap indices. NVDA respectively enjoys weights of 8.8 percent and 8.4 percent in QQQ (Invesco QQQ Trust) and SPY (SPDR S&P 500 ETF).

Shares of NVDA dropped 4.4 percent for the week, and a sustained downward pressure is bound to adversely impact the Nasdaq 100, for instance. Despite NVDA’s problems, the tech-heavy index managed to add 1.2 percent this week to 29482. This was the seventh up week in eight, with last week’s loss of 0.4 percent helping form a weekly spinning top. This week, with a low of 28567 on Tuesday, a potentially bearish hanging man has formed, although it needs confirmation. Next week is key, as Tuesday’s low is a must-hold.

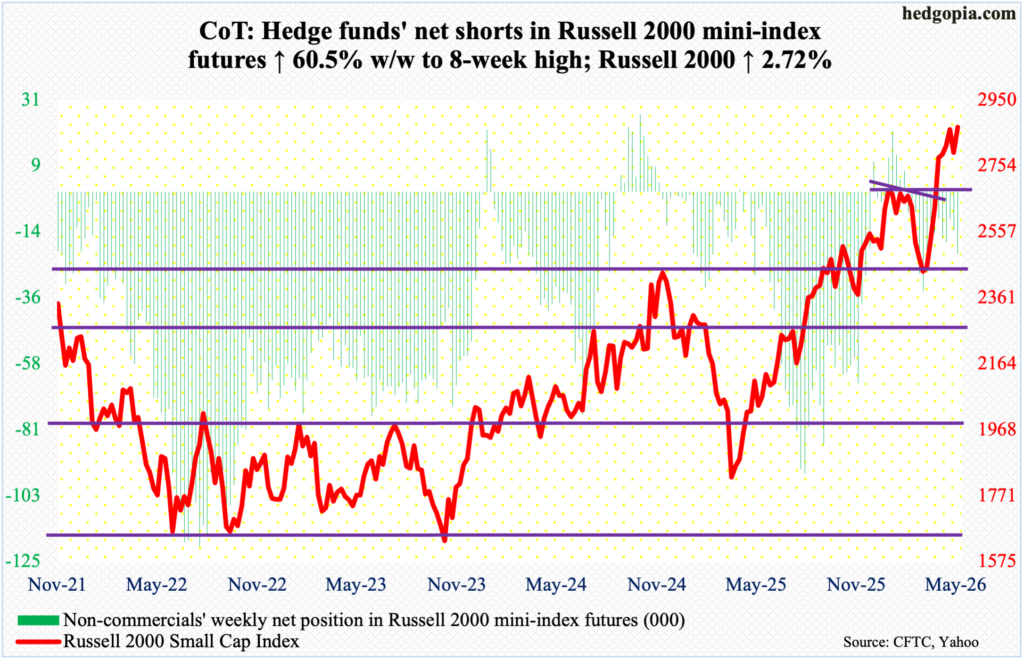

Russell 2000 mini-index: Currently net short 21k, up 7.9k.

The week belonged solidly to small-cap bulls, yet the bears had their share of success, if it can be called that. The latter succeeded in stopping the bulls at 2880s, with Friday tagging 2883 and the week finishing up 2.7 percent to 2869. This was third week in a row the Russell 2000 ticked 2880s – 2889 on the 7th and 2888 on the 11th.

For their part, bulls just about enjoyed a successful breakout retest. On January 27, the Russell 2000 peaked at 2735 – a level that was reclaimed six weeks ago, followed by a successful retest four weeks ago. Again, this week, there were bids waiting, as Tuesday’s session low 2747 was bought.

Next week, bulls and bears are set to wrestle over control of 2880s, with a slight edge to the former as things stand.

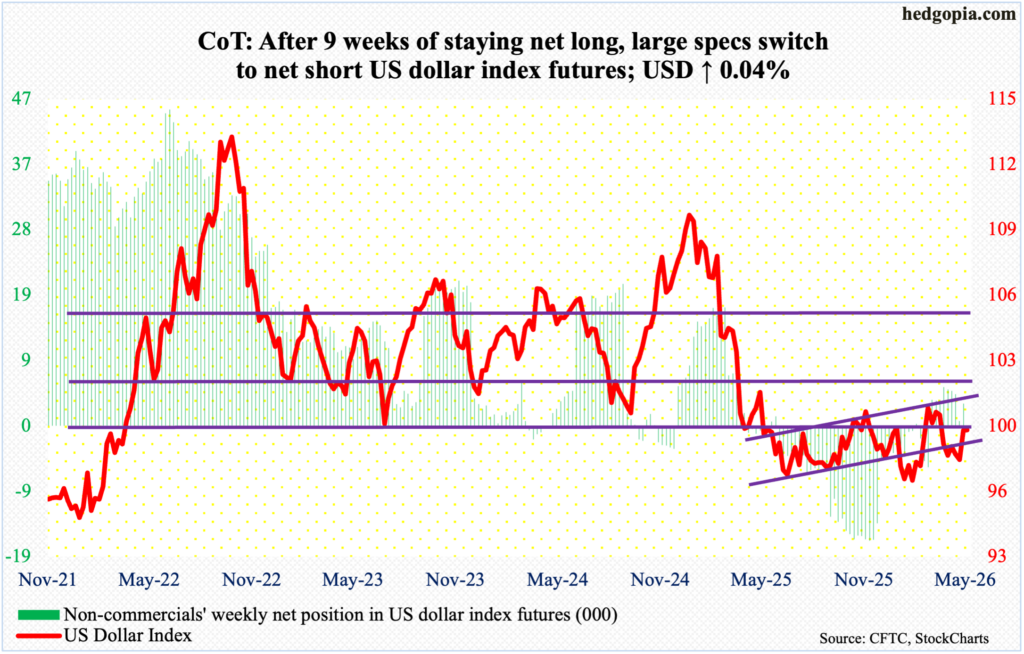

US Dollar Index: Currently net short 479, up 3.7k.

After having reclaimed the 200- and 50-day (98.57 and 98.96, in that order) on Thursday and Friday last week respectively, the US dollar index this week remained above the averages throughout, with the 50-day providing support in the first three sessions. At the same time, bulls were unable to hang on to all the gains, as the index had rallied as high as 99.52 on Thursday.

Last week, dollar bulls stepped up to defend horizontal support at 97.70s.

Markets are increasingly pricing in chances of a hike in the fed funds rate by the Federal Reserve, and this has helped the US dollar index, which is up 1.3 percent May-to-date.

Real test lies at 100, the significance of which goes back more than a decade, and which was lost in April last year. More recently, after unsuccessfully trying for five weeks to reclaim 100, including March 31 when an intraday high of 100.64 was hit intraday, dollar bulls gave up trying six weeks ago.

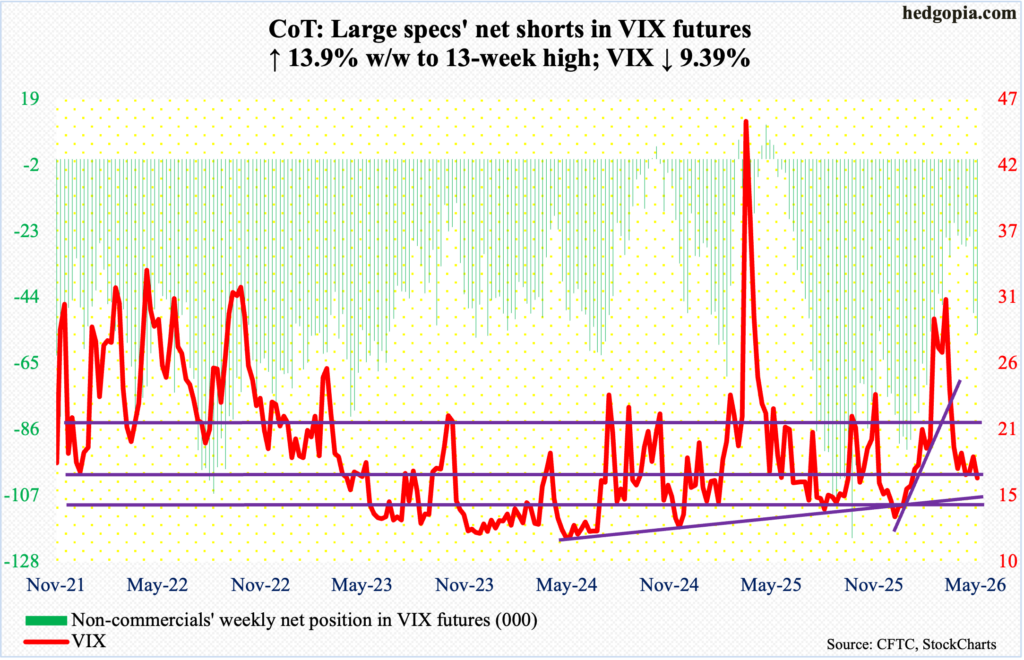

VIX: Currently net short 55.8k, up 6.8k.

Volatility bulls’ attempt to recapture the 200-day (18.35) failed as early as Monday. By the end of the week, VIX declined 9.4 percent to 16.70. There has been a lot of activity around this level for at least the past month. A breach will naturally raise the odds of a 15 handle.

This at a time when a ton of complacency is evident elsewhere in the options market. The CBOE equity-only put-to-call ratio has produced readings of 0.50s or lower, for 33 consecutive sessions, with 14 of them in the 0.40s.

Thanks for reading!