Following futures positions of non-commercials are as of March 7, 2017.

10-year note: The Janet Yellen-led Fed – and the one led by her predecessor Ben Bernanke – believe in the wealth effect. Since the financial crisis, anytime equities came under decent pressure, the Fed was there to help – verbally or through policy. Consequently, stocks knew when to throw a tantrum to get the Fed’s attention.

The Fed is set to hike next week. But stocks are not panicking. The real test takes place if come Wednesday Yellen hints that there will be at least two more hikes this year, let alone three. Composed market reaction would be a sign that they are no longer dependent on monetary morphine. And this makes the Fed’s job easier. Alternatively, markets throw a tantrum anyway, but the Fed in subsequent meetings looks the other way, which would be quite a development.

Currently net short 298.5k, down 111.1k.

30-year bond: Major economic releases next week are as follows.

FOMC meeting begins Tuesday and ends the next.

Tuesday also brings the NFIB optimism index (February) and PPI-FD (February).

Small-business optimism inched up one-tenth of a point month-over-month to 105.9 in January – the highest since December 2004. Last November through January, the index jumped 11 points. The post-election optimism is yet to translate to other sub-indexes, however. Comp plans fell a point to 18 in those three months.

Producer prices in January were up 0.6 percent m/m and up 1.6 percent in the 12 months through January. Core PPI rose 0.2 percent and 1.6 percent during the period, respectively.

On tap for Wednesday are CPI (February), retail sales (February), the NAHB housing market index (March), and the Treasury International Capital (January).

Consumer prices rose 0.6 percent m/m in January and 2.5 percent in the 12 months through January. Core CPI increased 0.3 percent and 2.2 percent during the period, respectively. This was the 15th consecutive year-over-year increase of north of two percent.

January retail sales were up 0.4 percent m/m to a seasonally adjusted annual rate of $472.1 billion. Sales jumped 5.6 percent y/y – the highest since 6.2 percent in March 2012.

February builder sentiment fell two points m/m to 65. Last December was 69, which was the highest since 70 in July 2005.

Foreigners sold $21.8 billion in Treasury notes and bonds last December. On a 12-month rolling total basis, they sold $342.8 billion worth in December, down from minus $356.8 billion in the prior month, which was a record.

Housing starts (February) and JOLTS (January) are due out on Thursday.

Housing starts dropped 2.6 percent m/m in January to a seasonally adjusted annual rate of 1.2 million units. The cycle high 1.32 million was reached last October – the highest since 1.33 million in August 2007.

Non-farm job openings fell 4,000 m/m in December to 5.5 million. Openings peaked at 5.85 million last April, essentially on par with 5.79 million in July 2015 and 5.83 million last July.

Industrial production (February) and the University of Michigan’s consumer sentiment index (March, preliminary) are published on Friday.

Industrial production inched up 0.01 percent y/y in January. This was the second straight y/y increase in the last 17 months. Similarly, capacity utilization in the last 23 months has only risen once, which occurred last December.

Consumer sentiment fell 2.2 points m/m in February. January’s 98.5 was a 13-year high.

Currently net short 42.8k, up 21k.

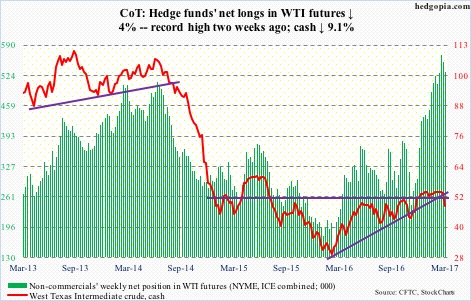

Crude oil: After trading sideways for 12 weeks during which non-commercials built the most net longs in West Texas Intermediate crude futures and U.S. crude inventory surged to one after another record, the bottom fell out this week, dropping 9.1 percent.

What was the trigger?

The EIA report for last week, out Wednesday, showed crude stock buildup continued, rising 8.2 million barrels to 528.4 million barrels. In the past nine weeks, inventory rose every week, for a cumulative 49.4 million barrels.

Crude imports rose, too, by 561,000 barrels per day to 8.2 million b/d. Ditto with crude production, which rose 56,000 b/d to 9.1 mb/d.

Refinery utilization, in the meantime, inched down one-tenth of a point to 85.9 percent.

Traders simply raised their hands and said ‘enough’. In the past several weeks, they focused on declining stocks of both gasoline and distillates, which respectively peaked at 259.1 million barrels (February 10, a new record) and 170.7 million barrels (February 3, highest since Oct 2010). Last week, they fell 6.6 million barrels to 249.3 million barrels and 2.7 million barrels to 161.5 million barrels, in that order. But the fact remains that stocks remain high.

All this probably contributed to trader reaction. In a matter of four sessions, the cash lost both 50- and 200-day moving averages. Depending on how one draws, the crude is either sitting on the rising trend line from the lows of February last year or lost it.

Bulls have their work cut out. Non-commercials are still massively net long.

Currently net long 532k, down 22k.

E-mini S&P 500: In the week ended Wednesday, U.S.-based equity funds attracted another $8.5 billion (courtesy of Lipper), but was no use. The S&P 500 (cash) lost 0.4 percent last week. The ones that began gravitating toward these funds in prior weeks are sitting pretty, though. Post-election, $60.6 billion went in, during which the S&P 500 rallied nearly 12 percent.

Incidentally, the bull this week completed eight years.

Similarly, SPY, the SPDR S&P 500 ETF, attracted $2.1 billion, and $23.4 billion post-election (courtesy of ETF.com).

This was the first down week in the last seven. Remains to be seen if this would act as a deterrent from the flows perspective. Thus far, the index is only 1.2 percent off the all-time high reached on March 1 (2400.98), but it is likely setting up for a bigger drop.

The cash has been under pressure since that record high. Last week’s reversal-like candle has been followed by this week’s hanging man.

Currently net long 137.6k, up 51k.

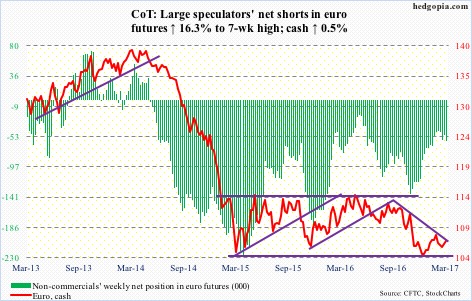

Euro: Mario Draghi’s, ECB president, statement Thursday that the euro was “irrevocable” was pretty much treated with a yawn in that session, followed then by a 0.9-percent jump on Friday, past the 50-day moving average.

Draghi by the way no longer sees a deflation risk in the Eurozone, at the same time says there are downside risks that could derail the recovery. Whatever! QE is here to stay, until at least December.

Meantime, euro bulls continue to defend support at 105-plus … 108 is the level to watch.

Currently net short 59.5k, up 8.3k.

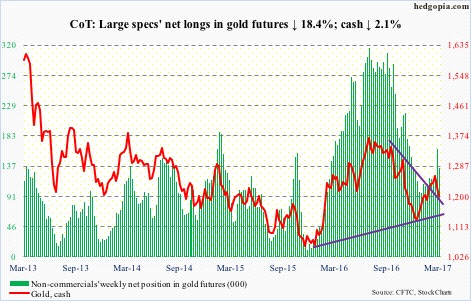

Gold: Gold bugs were unable to defend the 50-day moving average on the cash. The average is still rising, but shorter-term averages are now pointing lower. The metal ($1,201.40) also lost the rising trend line from the lows of last December, subsequent to which it rallied 12.5 percent.

There is support at $1,180 (intraday Friday, fell to $1,194.5). Let us see if that generates buying interest. In the week ended Wednesday, GLD, the SPDR gold ETF, lost $258 million (courtesy of ETF.com).

Currently net long 133.7k, down 30.1k.

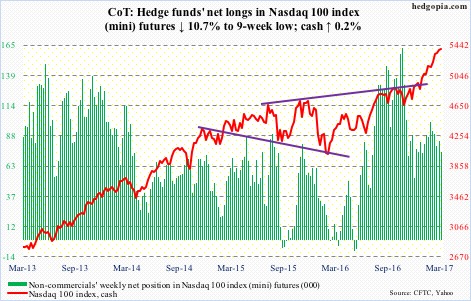

Nasdaq 100 index (mini): QQQ, the PowerShares Nasdaq 100 ETF, continues to attract money. In the week ended Wednesday, $412 million came in – third straight week of inflows (courtesy of ETF.com).

Bulls continue to defend the 10- and 20-day moving averages.

Short interest on XLK, the SPDR technology ETF, remains elevated.

Currently net long 74.8k, down 9k.

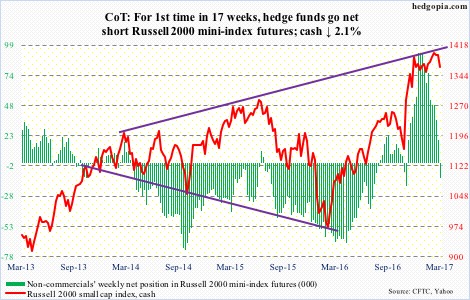

Russell 2000 mini-index: Of the four major U.S. indices (the other three being the S&P 500, Dow Industrials and the Nasdaq composite), the Russell 2000 (cash) is the first one to lose the 50-day moving average post-election.

In the week ended Wednesday, IWM, the iShares Russell 2000 ETF, lost $95 million (courtesy of ETF.com). This followed outflows of $1 billion in the prior two.

Bulls need to save 1347. A failure would mean overbought weekly conditions would continue to get unwound. (Fell to 1356.69 intraday Friday before finding bids.)

For the first time in 17 weeks, non-commercials are now net short.

Currently net short 12.3k, down 32k.

US Dollar Index: On December 15 last year, two-year T-notes yielded 1.29 percent, and the dollar index (cash) closed at 103.11. Thursday, they were respectively 1.37 percent and 101.72. The latter is having trouble keeping up. Either it does not believe the rise in two-year yields is sustainable or simply that a strong currency is not conducive to the U.S. economy, let alone emerging economies that are heavy in dollar debt.

At least near term, the cash is itching to go lower.

Currently net long 51.1k, up 6.2k.

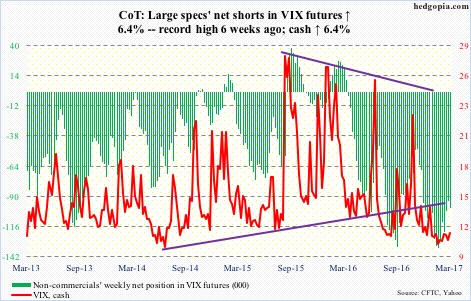

VIX: One more weekly doji on the cash – third in the last six weeks. In the meantime, the 50-day moving average is flat to slightly rising. With the average at 11.71, which itself is at the low end of a multi-year range, odds favor it begins to rise from here. That said, the 200-day is still dropping.

Currently net short 99.6k, up 6k.