Following futures positions of non-commercials are as of July 3, 2017.

10-year note: Currently net long 263k, down 39.1k.

The speed by which long rates rose the past couple of weeks took many by surprise. Intraday between June 26 and July 7, 10-year T-yields jumped from 2.12 percent to 2.4 percent.

Over in Germany and Japan, they doubled – of course from much lower levels. Between the periods, yields on German 10-year bunds went from 0.25 percent to 0.57 percent, and on 10-year JGBs from 0.05 percent to 0.10 percent on July 6.

Rates supposedly reacted to hawkish central-bank commentary, which has some truth to it. But they were also unwinding oversold technical conditions. Plus, at least as regards to 10-year U.S. Treasurys, non-commercials, still heavily net long, cut back holdings to a four-week low.

The bigger question is, if the current trajectory continues, how long before central banks start expressing displeasure? The Bank of Japan already did. Friday, it said it would buy an unlimited number of 10-year JGBs at a yield of 0.11 percent. The bank aims to pin 10-year yields at zero. Friday, yields fell to 0.09 percent.

They all have their own pain point, so will react differently. The one thing central banks in most developed economies – as well as in China – share is they are all dealing with leverage.

Take the U.S., for example.

In 1Q17, interest payments of the federal government were $508.9 billion (seasonally adjusted annual rate). At the end of the quarter, federal debt was $19.8 trillion. This equates to an effective interest rate of 2.56 percent. If rates go up by only one percent, interest payments would go up by just under $200 billion. This does not take into account state and local debt, not to mention corporate and household.

The amount of leverage out there would not allow a persistent rise in rates.

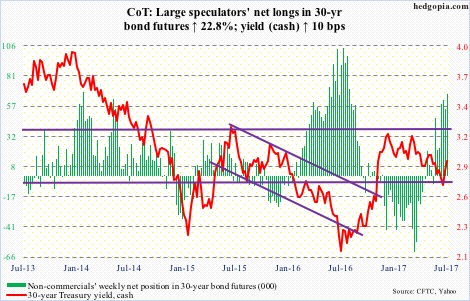

30-year bond: Currently net long 67k, up 12.4k.

Major economic releases next week are as follows.

The NFIB optimism index (June) and JOLTS (May) are scheduled for Tuesday.

Small-business optimism remained unchanged month-over-month in May at 104.5 – sixth straight monthly reading of north of 100. January’s 105.9 was a 12-year high. May job openings inched up a point to 34 – the highest since November 2000.

Non-farm job openings jumped 259,000 m/m in April to 6.04 million – a new record.

Thursday brings PPI-FD (June). Producer prices were flat in May. On a 12-month basis, prices rose 2.4 percent. Core PPI fell 0.1 percent, and rose 2.1 percent over 12 months.

On tap for Friday are CPI (June), retail sales (June), industrial production (June) and the University of Michigan’s consumer sentiment index (July, preliminary).

Consumer prices fell 0.1 percent m/m in May. In the 12 months through May, prices rose 1.9 percent. Core CPI rose 0.1 percent and 1.73 percent, respectively. This was the second straight sub-two-percent year-over-year increase after rising north of two percent for 17 straight months.

Retail sales fell 0.3 percent m/m in May to a seasonally adjusted annual rate of $473.8 billion. They rose 3.8 percent y/y, decelerating from growth of 5.6 percent this January.

Capacity utilization rose 1.4 percent y/y to 76.6 percent in May. This was the third straight month following 24 down months out of 25. Utilization reached cycle high 79.2 percent last November.

Consumer sentiment fell two points m/m in June to 95.1. January’s 98.5 was a 13-year high.

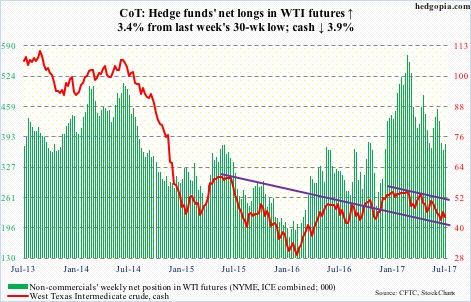

Crude oil: Currently net long 377.8k, up 12.5k.

The same way spot West Texas Intermediate crude bounced off support two weeks ago, the subsequent rally got repelled at resistance this week.

There was horizontal support at $42-plus going back nearly two and a half years. This also represented the neckline of a head-and-shoulders formation plus a failing trend line from last October.

From the intraday low of $42.05 on June 21 to Wednesday’s high of $47.32, the crude quickly rallied 12.5 percent. The 50-day moving average lies at $46.88. Plus, $47 faces horizontal resistance going back at least three months.

The crude is looking to digest the recent gains. Friday, bulls were unable to defend shorter-term moving averages.

The latest EIA report contained more positives than negatives, but that was no help.

In the week ended June 30, stocks fell across the board – crude down 6.3 million barrels to 502.9 million barrels, gasoline down 3.7 million barrels to 237.3 million barrels, and distillates down 1.9 million barrels to 150.4 million barrels.

Crude imports were down 274,000 barrels/day to 7.74 million b/d.

Refinery utilization rose 1.1 percentage points to 93.6 percent.

Crude production, on the other hand, rose 88,000 b/d to 9.34 mb/d.

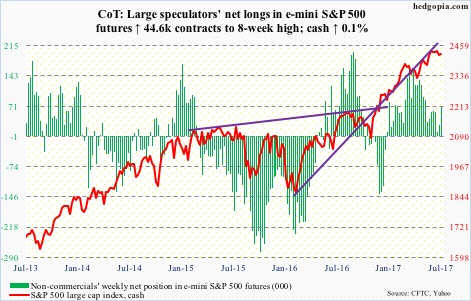

E-mini S&P 500: Currently net long 69.6k, up 44.6k.

Kudos to the bulls for saving the week. Down 0.6 percent at one point, the cash ended up 0.07 percent. The 50-day as well as 2400 was tested for the second straight week, and held – for now. It is longs’ ball to lose, at least near term.

That said, at least until Wednesday, flows were not cooperating.

In the week ended that session, U.S.-based equity funds lost another $3.3 billion – now down $15.2 billion in the past three weeks (courtesy of Lipper).

In the same week, IVV (iShares core S&P 500 ETF) and VOO (Vanguard S&P 500 ETF) together took in $790 million – $609 million and $181 million, respectively. But SPY (SPDR S&P 500 ETF) experienced bigger redemptions – $2.2 billion (courtesy of ETF.com).

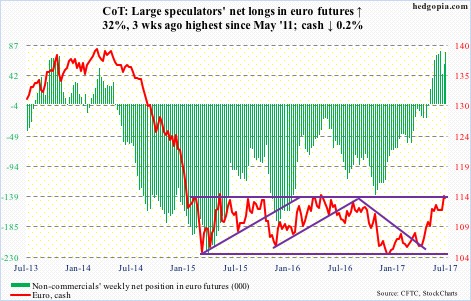

Euro: Currently net long 77.5k, up 18.8k.

The recent break out of 113 was just about tested Wednesday when the cash bounced off the still-rising 10-day.

The euro has essentially been trapped in a rectangle for two and a half years, and is currently at the top of the range. A genuine breakout here will be huge.

Nonetheless, the bulls have already expended a lot of energy in rallying the currency 11 percent in the past seven months. Plus, markets likely have already priced in a potentially hawkish message from the ECB in the weeks and months ahead.

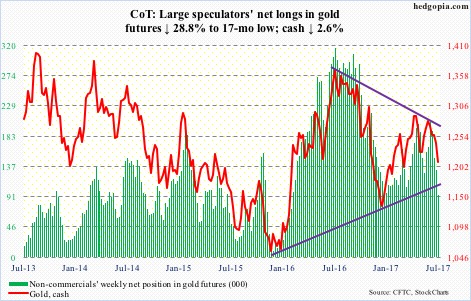

Gold: Currently net long 93.8k, down 37.9k.

After trading between the 50- and 200-day for 12 sessions, the cash ($1,209.7) lost the latter Monday when it lost 1.9 percent. It is now below a rising trend line from last December.

The loss of both the averages likely unnerved many.

In the week to Wednesday, GLD (SPDR gold ETF), lost $518 million (courtesy of ETF.com). This was the largest weekly withdrawal since last December.

Non-commercials’ net longs are at a 17-month low.

The daily chart is oversold. A rally, should it happen, likely attracts sellers around the 200-day ($1,236.08).

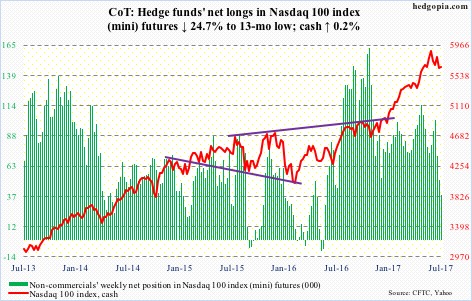

Nasdaq 100 index (mini): Currently net long 38.6k, down 12.6k.

The cash is trying to push off of the bottom of a short-term channel – an opportunity for the bulls to step up to the plate. But flows are not cooperating.

In the week through Wednesday, $1.4 billion was withdrawn from QQQ (PowerShares Nasdaq 100 ETF). In the prior four, $1.5 billion came out.

The Nasdaq 100 (5656.47) lost the 50-day last week, as it did the rising trend line from last November. The average is one percent away. Failure to recapture it ultimately exposes the index to breakout retest at 5450.

Russell 2000 mini-index: Currently net short 18k, up 1.4k.

The bulls and bears continue to fight over control of shorter-term averages on the cash, with the former struggling at 1420s for several weeks. Thursday’s 1.4-percent drop also tested the 50-day – now flat to slightly down – and held.

Nonetheless, the weekly chart has produced a back-to-back long-legged doji.

Near-term, the bulls’ real test lies in if they can save 1390s. The Russell 2000 went sideways between 1340s and 1390s for months before a breakout five weeks ago.

At least in the week ended Wednesday, funds were uncooperative, with IWM (iShares Russell 2000 ETF) losing $472 million (courtesy of ETF.com). This followed redemptions of $810 million in the prior week.

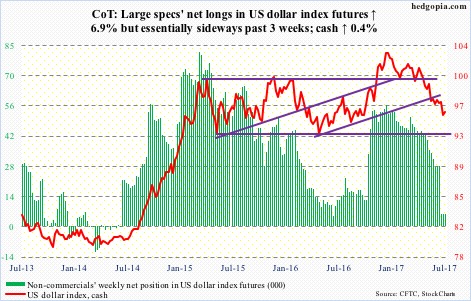

US Dollar Index: Currently net long 5.8k, down 378.

The cash did not even get to test 96.50-ish, as it was rejected at 96.26 just under the 10-day, which, along with the 20-day, need to stabilize for the dollar index to begin to unwind oversold conditions.

Medium term, the path of least resistance is up.

All the better if non-commercials begin to accumulate net longs, which have gone flat the past three weeks.

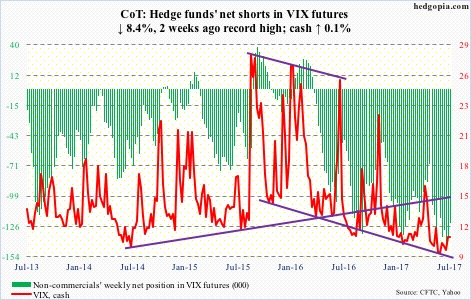

VIX: Currently net short 123.6k, down 11.4k.

For the second week running, the cash (11.19) went after the 200-day. Unlike last week, it took it out Thursday, only to lose it the next – has room to go lower on the daily chart.

Medium-term, the 50-day (10.75) is now flat to slightly up – potentially important development should it hold.

Thanks for reading! Please share.