The following are futures positions of non-commercials as of September 1, 2015. Change is week-over-week.

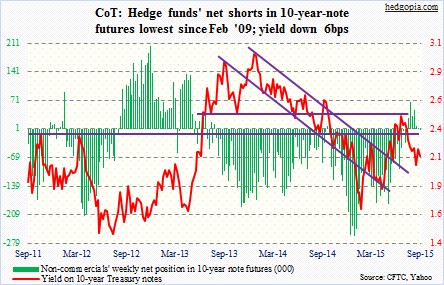

10-year note: The IMF is at it again. This week, it reiterated its stance that advanced economies should maintain accommodative monetary policies. By that it essentially means the Fed, which it urged in July to hold off on raising rates until next year.

Even if the Fed gives the IMF the cold shoulder, the August jobs report has probably given fodder to both the doves and hawks within the FOMC. Only 173,000 non-farm jobs were added, but June and July were revised higher by a combined 58,000. The unemployment rate slid further to 5.1 percent – lowest since April 2008 (five percent) – but more Americans are opting out of the labor force. When the recovery began six-plus years ago there were 81 million in the ‘not in labor force’ category, now they total 94 million. As well, private-sector average hourly earnings increased by better-than-expected $0.08 in August, but annual growth is still stuck in the two-percent range.

Is it any wonder that FOMC members are as divided as they are? At Jackson Hole, Stanley Fischer, Fed vice chair, hinted a September hike is still on the table. A few days before that, Bill Dudley, president of the New York Fed, was not so sure. Perhaps it is up to Chair Janet Yellen to break the tie.

Reacting to the jobs report on Friday, the two-year Treasury yield rose three basis points to 0.71 percent – as if a hike is imminent in two weeks. Although the long end of the curve failed to go along. TLT, the iShares 20+ Year Treasury ETF, rallied 0.9 percent. A resulting flatter curve seems worried that a hike will hurt the economy more than help. The Fed has missed a window of opportunity to hike.

Non-commercials are as confused as FOMC members. They are essentially straddling the line – could go either way from here.

Currently net short 2.8k, up 4.1k.

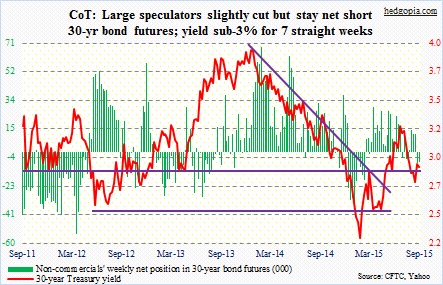

30-year bond: Here are the major economic releases next week. Happy Labor Day!

The NFIB small business optimism index is published on Tuesday. July was 95.4, up 1.3 points month-over-month. The index has been under pressure since the recovery high of 100.4 reached last December.

July’s JOLTS report is due out on Wednesday. Non-farm job openings were 5.25 million in June, down from the all-time high of 5.36 million in May. This series tends to correlate with/lead non-farm jobs. Also, quits peaked at 2.78 million in January; June was 2.75 million. No biggie yet, but something to watch out for!

August’s producer price index for final demand comes out on Friday. In July, it rose 0.2 percent, down from 0.4 percent in June and 0.5 percent in May. In the 12 months through July, the PPI fell 0.8 percent, following a 0.7-percent decline in June – the sixth straight drop. Core PPI rose 0.2 percent in July, after rising 0.2 percent in June, and was up 0.9 percent in the 12 months through July. A subdued reading any way you look at it.

Also Friday is the University of Michigan’s consumer sentiment preliminary reading for September. August was 91.9, which was down from July’s 93.1 but up substantially from 82.5 year-over-year. Most recently, it peaked in January at 98.1.

No FOMC member is scheduled to speak next week.

Currently net short 6.7k, down 540.

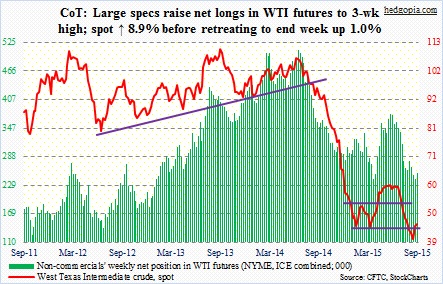

Crude oil: A double whammy! In the August 28th week, U.S. crude stocks rose by 4.7 million barrels, to 455.4 million barrels, and stocks of crude oil and refined products were up by 5.7 million barrels, to 1.289 billion barrels. Spot West Texas Intermediate crude totally ignored this, rallying 4.2 percent on Wednesday. Earlier on Monday, it rallied 6.3 percent before dropping 8.2 percent the next day.

By the time spot WTI retreated from the intra-day high of 49.33 on Monday, it had rallied 28 percent in three sessions! Too fast, too soon? Sellers did appear where they were supposed to. There is resistance at the 49-50 level. Besides, the 50-day moving average – still dropping – lies at 47.61. Just underneath, shorter-term moving averages have turned up. Near-term, WTI can come under pressure, and needs to hold 43.

Rather worryingly for bulls, the three-week spike has failed to coax non-commercials into action. They only added a tad to net longs.

Currently net long 254.1k, up 12.2k.

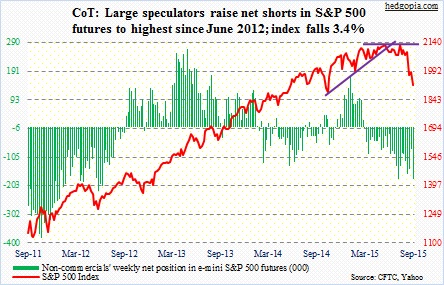

E-mini S&P 500: After massive $17.8 billion outflows in the August 26th week, equity funds continued to bleed in the September 2nd week, but at a much slower pace. A mere – relatively – $865 million was withdrawn, with domestic funds losing $1.6 billion and non-domestic funds attracting $746 million (courtesy of Lipper).

A sign of stability? Yes. However, for flows to stabilize, stocks need to stabilize. As long as the August 24th low on the S&P 500 is not breached, there is probably minimal risk of a pickup in outflows at this point in time. We could be looking at a different picture if those lows get taken out.

Between August 27th and September 3rd, American Association of Individual Investors bears dropped 6.6 points to 31.7 percent, while bulls were essentially flat at 32.4 percent. These retail investors obviously expect things to stabilize. Hence the significance of the August 24th low. Similarly, Investors Intelligence bulls dropped to 27.8 percent this week – the lowest since 26.4 percent in March 2009. Back then, the bulls’ count remained in the 20s for five straight weeks. In all those five weeks, bears were in the 40s, rising as high as 47.2 percent. This week, bears were 26.8 percent. In a worse-case scenario, there is plenty of room for transition from bulls/neutrals to bears.

Non-commercials, in fact, expect this – having raised net shorts to the highest since June 2012.

Currently net short 180.5k, up 104.8k.

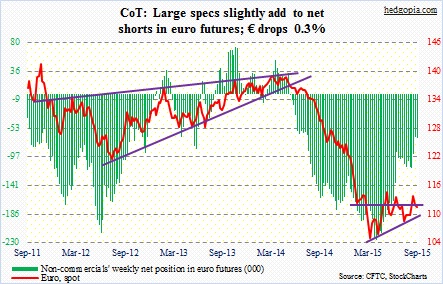

Euro: This Thursday was Mario Draghi’s, ECB president, 68th birthday. European markets in particular were handed out a celebratory cake – so to speak. If the need be, there will be more stimulus, Mr. Draghi suggested. European bourses rallied strongly that day.

Both inflation and GDP forecasts for the Eurozone have been revised downward. Inflation forecast went from previous 0.3 percent rise to 0.1 percent rise this year, from 1.5 percent to 1.1 percent next year and from 1.8 percent to 1.7 percent in 2017, while GDP is now forecast to grow 1.4 percent this year, 1.7 percent next year and 1.8 percent in 2017.

The likelihood of the ECB stepping up its current €60 billion/month asset purchases – both size and duration – has risen. Mr. Draghi said asset purchases are intended to run until the end of September 2016, or beyond, if necessary. The ECB also increased the bond purchase limit – from 25 percent to 33 percent – which will increase the outstanding stock of QE-eligible bonds.

So far so good. He has succeeded in talking down the euro, which fell 0.9 percent on Thursday, followed by a 0.2-percent rise on Friday. By the way, Eurozone PMI was 54.3 in August, versus an earlier estimate of 54.1. Nonetheless, Mr. Draghi – and Germany, in particular – are probably not happy with the euro’s direction. Between the March 9th low of 104.62 and the August 24th high of 117.14, it has rallied 12 percent.

Prior to Mr. Draghi’s dovish comments, non-commercials only slightly added to net shorts, which are substantially below the March highs.

Currently net short 67.9k, up 1.8k.

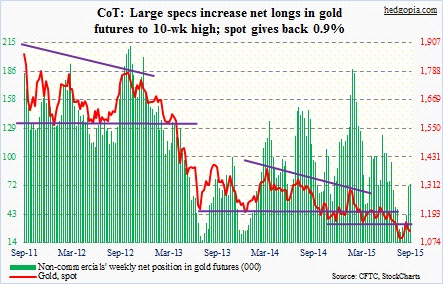

Gold: Gold bugs are probably disheartened by the metal’s inability to rally on Mr. Draghi’s comments. Technically, gold’s path of least resistance was already down in the near-term. Nonetheless, one would think news of more money-printing would help the metal.

Having said that, non-commercials continue to build net longs. They have now added for five straight weeks.

Currently net long 72.7k, up 2k.

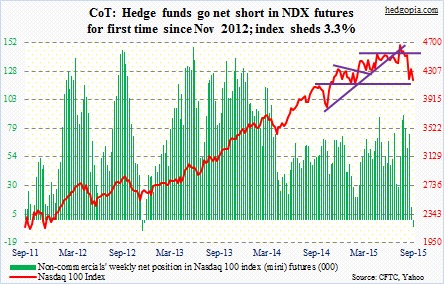

Nasdaq 100 index (mini): As of July 28th, non-commercials were net long just a tad over 90,000 contracts. Then they started to cut back, with a mere 11,000-plus last week. This week, they have one-upped that. For the first time since November 2012, they are now net short.

The good thing – if you are a bull – is that on Tuesday buyers stepped up to defend support at 4100. It is a must-hold. The 50-day moving average is rapidly approaching the 200-day moving average from above. A mere 68 points separate the two. Of the major U.S. indices, it, along with the Nasdaq Composite, is the only one not to have suffered a death cross.

Currently net short 6.1k, down 17.5k.

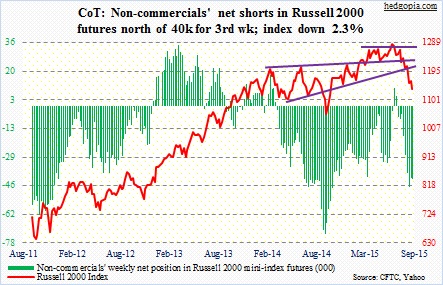

Russell 2000 mini-index: Non-commercials are not showing the same aggressive bearish bias on the Russell 2000 as they have on the S&P 500 and the Nasdaq 100. For the week, net shorts were essentially flat. It is possible they decided to stay pat with what they have, as they had already built sizable net shorts, which for the third straight week were in excess of 40,000 contracts. But the fact that they are not adding is beginning to get reflected on the price. For the week, the Russell 2000 was down 2.3 percent, against a 3.4-percent drop in S&P 500.

Currently net short 41.8k, up 441.

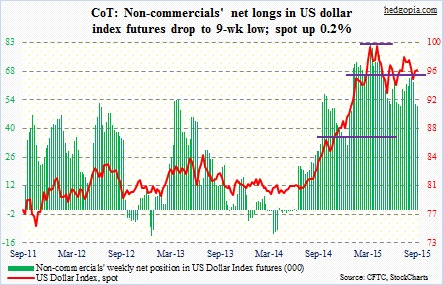

US Dollar Index: This week’s holdings would not tell us a lot. Next week’s will. Post-Mr. Draghi’s dovish comments, we would not know until next week non-commercials’ reaction to what is now looking like inevitable expansion in Eurozone QE. So far, they have continued to trim net longs.

A strong dollar has already taken its toll on U.S. exports; the latter’s share in nominal GDP dropped to 12.7 percent in 2Q15 from 13.7 percent 4Q13. The dollar index spiked 26 percent between July last year and March this year.

Welcome to a currency war – open or stealth.

Currently net long 51.2k, down 1k.

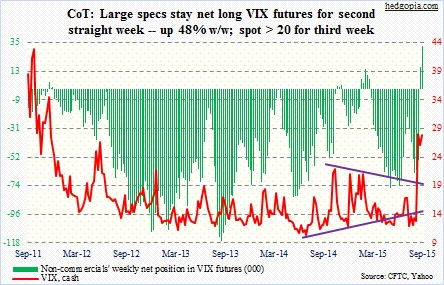

VIX: Spot VIX remained north of 20 for the third straight week, although it is substantially below the August 24th panic peak of 53.29. The CBOE did brisk business in that panicky atmosphere. Total volume in VIX futures for August was 6.4 million contracts, up 28 percent month-over-month and 41 percent year-over-year. The month also included VIX weekly contracts, which were launched on July 23rd, but the increase in activity is reflective of the prevailing investor mood in the bottom third of August.

Where to from here? Non-commercials were right to have gone net long last week, and they are at it again, raising net longs by 48 percent and staying net long for the second consecutive week.

Currently net long 32.2k, up 15.4k.

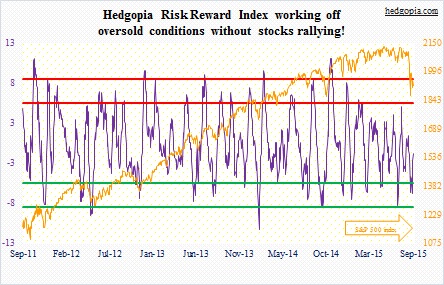

Hedgopia Risk Reward Index