Following futures positions of non-commercials are as of June 20, 2017.

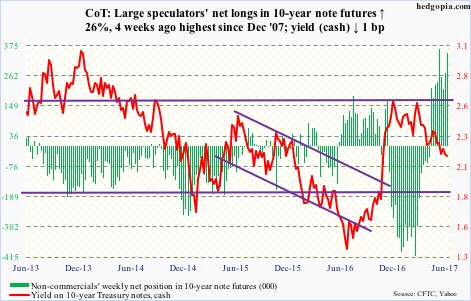

10-year note: Currently net long 345.2k, up 71.2k.

Last week, 10-year T-yields lost – albeit ever so slightly – a rising trend line from last July. Back then, yields bottomed at the all-time low of 1.34 percent. This week’s high of 2.19 percent got repelled at the underside of that broken trend line.

Yields have been under pressure since mid-March this year when they unsuccessfully tested multi-year resistance at 2.62 percent.

Post-presidential election in November last year, there were two gap-ups – one on the 9th and the other on the 14th that month. Last week’s low of 2.1 percent fills the first gap. The second one does not get filled until 1.87 percent. This is a worse-case scenario for bond bears – and music to the ears of non-commercials.

These traders switched from being net short 10-year note futures to net long in the week ended April 25. By May 23, they held 362,501 net longs – the highest since December 2007 – and have been rewarded.

30-year bond: Currently net long 61.6k, up 2.8k.

Major economic releases next week are as follows.

Durable goods for May are on tap for Monday. Orders for non-defense capital goods ex-aircraft – proxy for business capital expenditures – rose three percent year-over-year in April to a seasonally adjusted annual rate of $62.9 billion. Orders peaked in September 2014 at $70.3 billion.

April’s S&P Corelogic Case-Shiller U.S. home price index comes out Tuesday. Nationally, prices increased 5.8 percent y/y in March. This was the 59th consecutive month of y/y increase.

May’s pending home sales index will be published Wednesday. April was down 1.5 points m/m to 109.8. The cycle high – and a 10-year high – 113.6 was reached in April last year.

GDP (1Q17, final) and corporate profits (1Q17, revised) are scheduled for Thursday.

The second estimate showed the economy grew at an annual rate of 1.2 percent in 1Q17 – the slowest pace since 0.8 percent in 1Q16.

Preliminarily, 1Q17 corporate profits with inventory valuation and capital consumption adjustments grew 3.7 percent y/y to $2.11 trillion (SAAR). Profits peaked at $2.22 trillion in 4Q14.

Friday brings personal income and outlays (May) and the University of Michigan’s consumer sentiment index (June, final).

Core PCE (personal consumption expenditures) – the Fed’s favorite measure of consumer inflation – rose 1.54 percent y/y in April. In January, prices were rising at 1.79 percent. That said, the last time they rose north of two percent was in April 2012.

Consumer sentiment fell 2.5 points m/m in June to 94.5. The post-election euphoria is being worked off. In October last year, sentiment read 87.2, then jumping to 98.5 by January – a 13-year high.

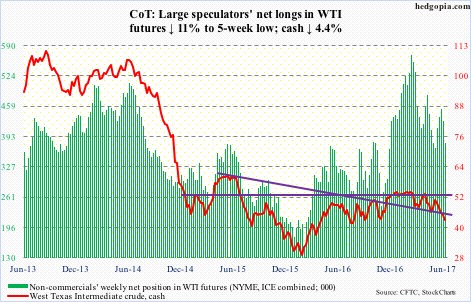

Crude oil: Currently net long 379.5k, down 46.7k.

Wednesday’s EIA report was not that bad, but spot West Texas Intermediate crude fell another 2.3 percent in that session anyway.

Technicals are broken, with the crude ($43.01) literally sitting on the neckline of a head-and-shoulders formation. The $42-plus level also represents horizontal support going back nearly two and a half years plus a failing trend line from last October.

Bulls need to step up to the plate. Action on Thursday and Friday is encouraging, with the daily MACD at a level when it bottomed this March and May. Even under this scenario, it will take time before the crude stabilizes.

In the week ended June 16, crude stocks dropped 2.5 million barrels to 509.1 million barrels – a 19-week low. As did gasoline inventory, which fell 578,000 barrels to 241.9 million barrels.

Crude imports fell, too – by 149,000 barrels/day to 7.88 million b/d – a six-week low.

Distillate stocks, on the other hand, rose 1.1 million barrels to 152.5 million barrels – a 12-week high.

Refinery utilization fell four-tenths of a point to 94 percent.

Last but not the least, crude production rose 20,000 b/d to 9.35 mb/d. Since OPEC reached a cutback agreement late November last year, production has increased by 651,000 b/d.

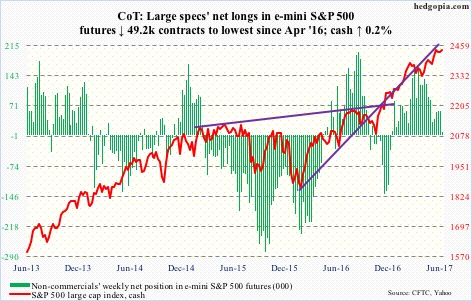

E-mini S&P 500: Currently net long 8.6k, down 49.2k.

The tug of war continued between bulls and bears around 10- and 20-day moving averages on the cash. The latter – slightly rising – was defended twice this week, and twice last week. If the sideways action continues, a cross-under is possible, which should swing near-term odds in bears’ favor.

Even in this scenario, bulls have support at 2400, which also approximates the 50-day. Flows likely decide what happens next should the support get tested.

In the week to Wednesday, SPY (SPDR S&P 500 ETF) gained $444 million (courtesy of ETF.com). But IVV (iShares core S&P 500 ETF) and VOO (Vanguard S&P 500 ETF) together lost $2.5 billion – $2.3 billion and $178 million, respectively.

In the same week, $2.2 billion was withdrawn from U.S.-based equity funds (courtesy of Lipper).

For whatever it is worth, corporate buybacks continue to decelerate.

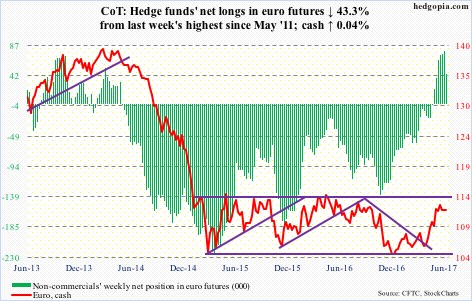

Euro: Currently net long 44.9k, down 34.2k.

The cash (111.93) is trapped between overbought weekly and oversold daily technicals.

Tuesday, bears pushed the euro under support at 111.6 to all the way down to 111.19 but not much followed from that action. Come Friday, bulls wrested control of that support-turned-resistance.

If weekly conditions prevail, the next level to watch is gap support at 110.5. The 50-day (110.45) lies right around there.

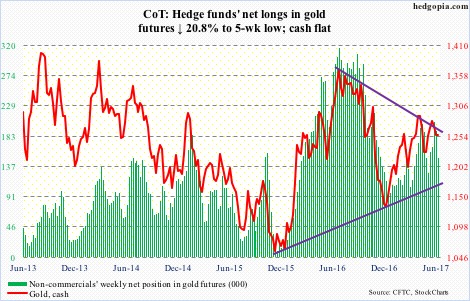

Gold: Currently net long 150.7k, down 39.6k.

The cash is currently sandwiched between 50- and 200-day, with the latter providing support early in the week and the former providing resistance on Friday.

Gold ($1,256.4) has come under pressure since it met with resistance at the $1,300 level three weeks ago. So this is an opportunity for gold bugs to break out of the 50-day. There is room to rally on the daily chart.

Defense this week of the 200-day also approximates a rising trend line from last December, hence its significance.

At least until Wednesday, as the metal was testing support, flows were not coming in. In the week ended Wednesday, GLD (SPDR gold ETF), lost $37 million (courtesy of ETF.com).

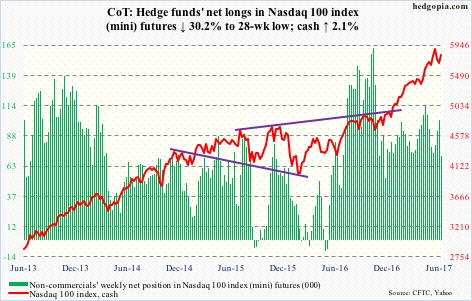

Nasdaq 100 index (mini): Currently net long 70.9k, down 30.6k.

The week produced a little something for both bulls and bears. The former was able to rally the cash (5803.11) off of the 50-day, which was defended last week. As well, the 20-day has been captured.

That said, subtle signs of fatigue are beginning to show up. After seven straight up months, June, with five sessions to go, has produced a long-legged doji. The all-time high of 5897.69 on June 9 stands.

QQQ (PowerShares Nasdaq 100 ETF) in the week ended Wednesday lost $239 million, following redemptions of $486 million in the prior week (courtesy of ETF.com).

Russell 2000 mini-index: Currently net short 15.4k, down 22.9k.

In the week ended Wednesday, IWM, the iShares Russell 2000 ETF, attracted $145 million (courtesy of ETF.com). This was the fourth straight weekly flows totaling $3 billion, $2.4 billion of which came in the last two.

Incidentally, the cash peaked on June 9 at 1433.79. Thus, IWM flows the past couple of weeks have been under water. Remains to be seen if this ends up impacting flows going forward.

Equally important is if longs will be able to forge a successful breakout retest whenever one occurs. Thursday came close. Prior to a breakout three weeks ago, the Russell 2000 went sideways between 1340s and 1390s for six months. The top of the range also approximates the 50-day (1393.03).

So far, so good. Bulls defended the 20-day and reclaimed the 10-day this week.

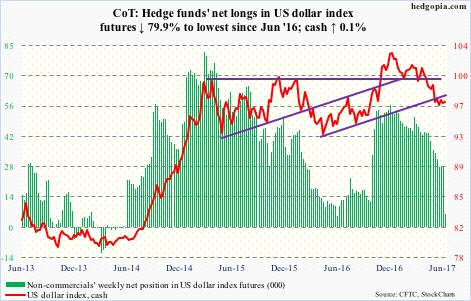

US Dollar Index: Currently net long 5.6k, down 22.4k.

On the weekly chart, there is room for the cash to rally. The daily on the other hand is beginning to look a little stretched, with the cash (96.94) not able to break out of near-term resistance at 97.3. A breakout here would have opened the door for a test of the 50-day at 98.05. Daily Bollinger bands have tightened, which usually precedes a sharp move one way or the other.

Non-commercials continue to show disinterest, with net longs lowest since June 2016.

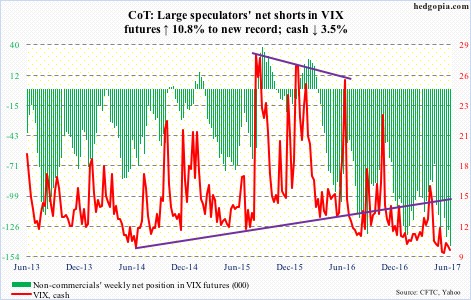

VIX: Currently net short 143.8k, up 14k.

Yet another week and yet another instance of the now-dropping 50-day resisting a rally attempt by the cash. And yet another week of a sub-10 reading, which occurred intraday Friday.

At the same time, bulls are defending the low end of a multi-year range VIX is in.

So the saga continues, with volatility bears staying with their massive net shorts and bulls longing for a squeeze.

Non-commercials are the most net short ever, even as in the week to Wednesday, VXX (iPath S&P 500 VIX short-term futures ETN) took in $40 million. This followed inflows of $98 million in the prior two (courtesy of ETF.com).

Thanks for reading! Please share.